Tame Case Study PIR Exhibits

Tame Book Case Study Results

Exhibits by Chapter

- Chapter 2: Basic loss statistics (A-C)

- Chapter 4: VaR, TVaR and EPD statistics (D, E)

- Chapter 7: Portfolio pricing, used for calibration (F, G)

- Chapter 9: Classical portfolio and stand-alone pricing (H-L)

- Chapter 11: Modern portfolio and stand-alone pricing (M-Q)

- Chapter 13: Classical allocations (R, S)

- Chapter 15: Modern allocations (T-Y)

See Section 1.28 for more details.

Table A

PIR Chapter 2, Tables 2.3, 2.5, 2.6, 2.7, Estimated mean, CV, skewness and kurtosis by line and in total, gross and net.

| statistic | Gross: A | Gross: B | Gross: Total | Net: A | Net: B | Net: Total |

|---|---|---|---|---|---|---|

| Mean | 50 | 50 | 100 | 50 | 49.084 | 99.084 |

| CV | 0.1 | 0.15 | 0.09 | 0.1 | 0.123 | 0.079 |

| Skewness | 0.2 | 0.3 | 0.207 | 0.2 | -0.484 | -0.169 |

| Kurtosis | 0.06 | 0.135 | 0.07 | 0.06 | -0.474 | -0.157 |

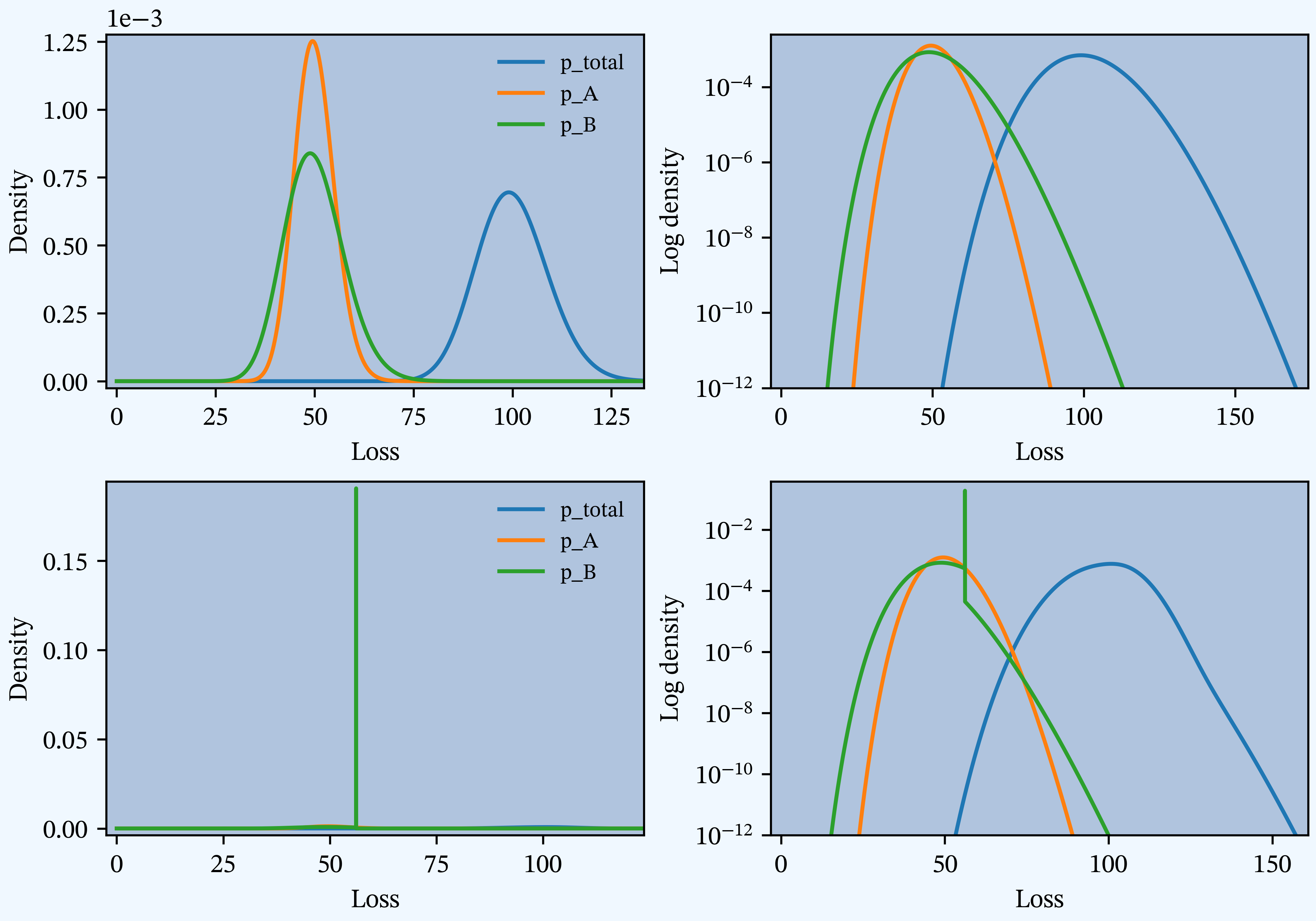

Figure B

PIR Chapter 2, Figures 2.2, 2.4, 2.6, Gross and net densities on a linear and log scale.

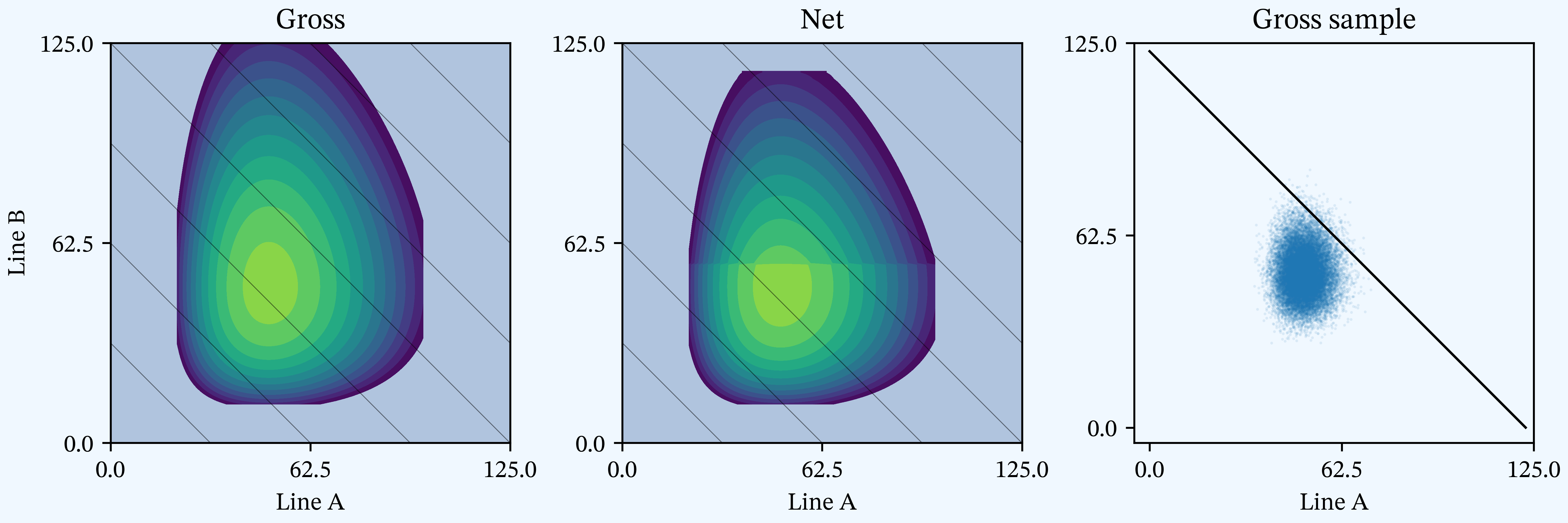

Figure C

PIR Chapter 2, Figures 2.3, 2.5, 2.7, Bivariate densities: gross and net with gross sample.

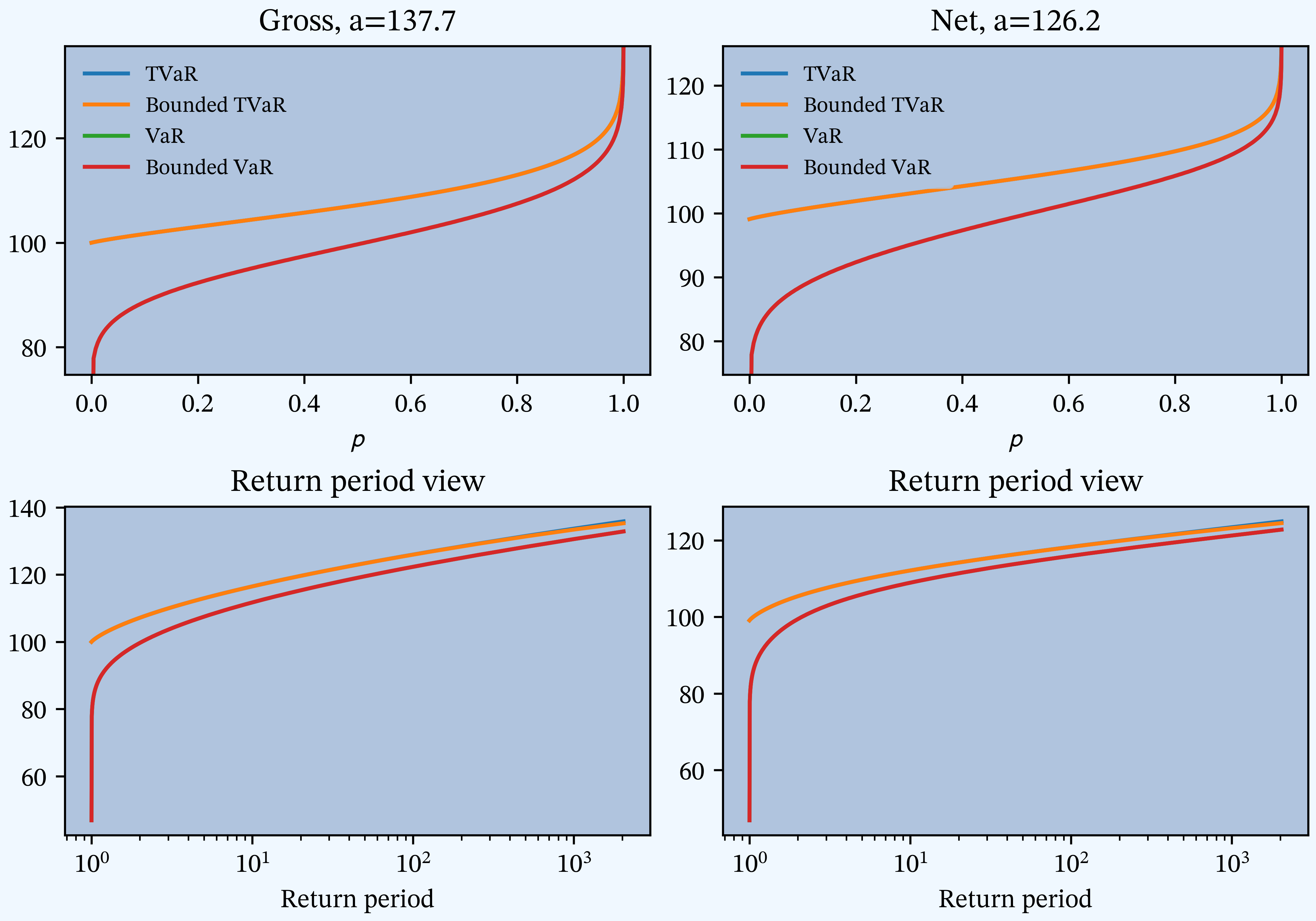

Figure D

PIR Chapter 4, Figures 4.9, 4.10, 4.11, 4.12, TVaR, and VaR for unlimited and limited variables, gross and net.

Table E

PIR Chapter 4, Tables 4.6, 4.7, 4.8, Estimated VaR, TVaR, and EPD by line and in total, gross, and net.

| statistic | Gross: A | Gross: B | Gross: Benefit | Gross: Sum | Gross: Total | Net: A | Net: B | Net: Benefit | Net: Sum | Net: Total |

|---|---|---|---|---|---|---|---|---|---|---|

| VaR 90.0 | 56.5 | 59.8 | 0.041 | 116.3 | 111.7 | 56.5 | 56.2 | 0.0344 | 112.7 | 108.9 |

| VaR 95.0 | 58.5 | 62.9 | 0.053 | 121.4 | 115.3 | 58.5 | 56.2 | 0.0296 | 114.7 | 111.4 |

| VaR 97.5 | 60.3 | 65.7 | 0.063 | 126 | 118.5 | 60.3 | 56.2 | 0.026 | 116.4 | 113.5 |

| VaR 99.0 | 62.4 | 69.1 | 0.0743 | 131.4 | 122.3 | 62.4 | 56.2 | 0.0224 | 118.5 | 115.9 |

| VaR 99.6 | 64.3 | 72.1 | 0.0843 | 136.4 | 125.8 | 64.3 | 59.2 | 0.0452 | 123.5 | 118.2 |

| VaR 99.9 | 66.9 | 76.4 | 0.0974 | 143.3 | 130.6 | 66.9 | 63.5 | 0.0754 | 130.4 | 121.2 |

| TVaR 90.0 | 59.1 | 64 | 0.0568 | 123.1 | 116.5 | 59.1 | 56.5 | 0.0314 | 115.6 | 112.1 |

| TVaR 95.0 | 60.9 | 66.7 | 0.0664 | 127.6 | 119.6 | 60.9 | 56.8 | 0.0307 | 117.7 | 114.2 |

| TVaR 97.5 | 62.4 | 69.2 | 0.075 | 131.7 | 122.5 | 62.4 | 57.5 | 0.0333 | 119.9 | 116 |

| TVaR 99.0 | 64.4 | 72.3 | 0.0849 | 136.7 | 126 | 64.4 | 59.4 | 0.0463 | 123.8 | 118.3 |

| TVaR 99.6 | 66.1 | 75.2 | 0.0938 | 141.3 | 129.2 | 66.1 | 62.3 | 0.0666 | 128.4 | 120.4 |

| TVaR 99.9 | 68.6 | 79.2 | 0.106 | 147.8 | 133.7 | 68.6 | 66.3 | 0.0931 | 134.9 | 123.4 |

| EPD 10.0 | 45.5 | 46.5 | 0.0146 | 91.9 | 90.6 | 45.5 | 45.3 | 0.0122 | 90.8 | 89.7 |

| EPD 5.0 | 49 | 51.1 | 0.0277 | 100.1 | 97.4 | 49 | 49.2 | 0.0232 | 98.3 | 96 |

| EPD 2.5 | 51.8 | 54.8 | 0.0397 | 106.6 | 102.5 | 51.8 | 52 | 0.0323 | 103.7 | 100.5 |

| EPD 1.0 | 54.7 | 59 | 0.0536 | 113.8 | 108 | 54.7 | 54.2 | 0.0392 | 109 | 104.8 |

| EPD 0.4 | 57.2 | 62.7 | 0.0656 | 119.9 | 112.6 | 57.2 | 55.4 | 0.0407 | 112.6 | 108.2 |

| EPD 0.1 | 60.5 | 67.6 | 0.081 | 128.1 | 118.5 | 60.5 | 56.1 | 0.0374 | 116.5 | 112.3 |

Table F

PIR Chapter 7, Table 7.2, Pricing summary.

| stat | Gross | Net |

|---|---|---|

| Loss | 100 | 99.084 |

| Margin | 3.423 | 2.464 |

| Premium | 103.423 | 101.548 |

| Loss Ratio | 0.967 | 0.976 |

| Capital | 34.233 | 24.639 |

| Rate of Return | 0.1 | 0.1 |

| Assets | 137.656 | 126.188 |

| Leverage | 3.021 | 4.121 |

Table H

PIR Chapter 9, Tables 9.2, 9.5, 9.8, Classical pricing by method.

| method | Parameters: Value | A: Gross | B: Net | B: Gross | Total: Net | Total: Gross | Total: Ceded |

|---|---|---|---|---|---|---|---|

| Net | 50 | 49.1 | 50 | 99.1 | 100 | 0.916 | |

| Expected Value | 0.034 | 51.7 | 50.8 | 51.7 | 102.5 | 103.4 | 0.947 |

| Variance | 0.042 | 51.1 | 50.6 | 52.4 | 101.7 | 103.4 | 1.75 |

| Esscher | 0.041 | 51 | 50.5 | 52.4 | 101.5 | 103.4 | 1.92 |

| Exponential | 0.080 | 51 | 50.4 | 52.4 | 101.4 | 103.4 | 1.976 |

| Semi-Variance | 0.080 | 51.1 | 50.3 | 52.4 | 101.4 | 103.4 | 2.012 |

| VaR | 0.659 | 51.9 | 52.8 | 52.8 | 102.7 | 103.4 | 0.75 |

| Dutch | 0.953 | 51.9 | 51.5 | 52.8 | 102.1 | 103.4 | 1.327 |

| Standard Deviation | 0.380 | 51.9 | 51.4 | 52.8 | 102.1 | 103.4 | 1.362 |

| Fischer | 0.523 | 51.9 | 51.1 | 52.9 | 101.9 | 103.4 | 1.516 |

Table I

PIR Chapter 9, Tables 9.3, 9.6, 9.9, Sum of parts (SoP) stand-alone vs. diversified classical pricing by method.

| method | Total: Gross | Total: Net | SoP: Gross | SoP: Net | Delta: Gross | Delta: Net |

|---|---|---|---|---|---|---|

| Net | 100 | 99.1 | 100 | 99.1 | 0 | 0 |

| Expected Value | 103.4 | 102.5 | 103.4 | 102.5 | 0 | 0 |

| Variance | 103.4 | 101.7 | 103.4 | 101.7 | -0 | -0 |

| Esscher | 103.4 | 101.5 | 103.4 | 101.5 | 0 | 0 |

| Exponential | 103.4 | 101.4 | 103.4 | 101.4 | 0 | 0 |

| Semi-Variance | 103.4 | 101.4 | 103.5 | 101.4 | 0.054 | -0.029 |

| VaR | 103.4 | 102.7 | 104.7 | 104.7 | 1.234 | 1.984 |

| Dutch | 103.4 | 102.1 | 104.7 | 103.4 | 1.322 | 1.301 |

| Standard Deviation | 103.4 | 102.1 | 104.7 | 103.3 | 1.324 | 1.215 |

| Fischer | 103.4 | 101.9 | 104.8 | 103 | 1.355 | 1.14 |

Table J

PIR Chapter 9, Tables 9.4, 9.7, 9.10, Implied loss ratios from classical pricing by method.

| method | A: Gross | B: Net | B: Gross | Total: Net | Total: Gross | Total: Ceded |

|---|---|---|---|---|---|---|

| Net | 1 | 1 | 1 | 1 | 1 | 1 |

| Expected Value | 0.967 | 0.967 | 0.967 | 0.967 | 0.967 | 0.967 |

| Variance | 0.979 | 0.97 | 0.955 | 0.975 | 0.967 | 0.523 |

| Esscher | 0.98 | 0.973 | 0.954 | 0.976 | 0.967 | 0.477 |

| Exponential | 0.98 | 0.974 | 0.954 | 0.977 | 0.967 | 0.463 |

| Semi-Variance | 0.979 | 0.975 | 0.954 | 0.977 | 0.967 | 0.455 |

| VaR | 0.963 | 0.931 | 0.948 | 0.965 | 0.967 | 1.221 |

| Dutch | 0.963 | 0.953 | 0.946 | 0.97 | 0.967 | 0.69 |

| Standard Deviation | 0.963 | 0.955 | 0.946 | 0.971 | 0.967 | 0.672 |

| Fischer | 0.963 | 0.96 | 0.946 | 0.972 | 0.967 | 0.604 |

Table K

PIR Chapter 9, Table 9.11, Comparison of stand-alone and sum of parts premium.

| Gross SoP | Gross Total | Gross Redn | Net SoP | Net Total | Net Redn | |

|---|---|---|---|---|---|---|

| No Default: Loss | 100 | 100 | -0.0% | 99.1 | 99.1 | -0.0% |

| No Default: Premium | 104.9 | 103.4 | -1.4% | 102.9 | 101.5 | -1.3% |

| No Default: Capital | 48.7 | 34.2 | -29.7% | 37.8 | 24.6 | -34.8% |

| With Default: Loss | 100 | 100 | 0.0% | 99.1 | 99.1 | 0.0% |

| With Default: Premium | 104.9 | 103.4 | -1.4% | 102.9 | 101.5 | -1.3% |

| With Default: Capital | 48.7 | 34.2 | -29.7% | 37.8 | 24.6 | -34.8% |

Table L

PIR Chapter 9, Tables 9.12, 9.13, 9.14, Constant CoC pricing by unit for Case Study.

| Gross: A | Gross: B | Gross: SoP | Gross: Total | Net: A | Net: SoP | Net: Total | |

|---|---|---|---|---|---|---|---|

| No Default: Loss | 50 | 50 | 100 | 100 | 50 | 99.1 | 99.1 |

| No Default: Margin | 1.888 | 2.982 | 4.869 | 3.423 | 1.888 | 3.779 | 2.464 |

| No Default: Premium | 51.9 | 53 | 104.9 | 103.4 | 51.9 | 102.9 | 101.5 |

| No Default: Loss Ratio | 0.964 | 0.944 | 0.954 | 0.967 | 0.964 | 0.963 | 0.976 |

| No Default: Capital | 18.9 | 29.8 | 48.7 | 34.2 | 18.9 | 37.8 | 24.6 |

| No Default: Rate of Return | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| No Default: Leverage | 2.749 | 1.777 | 2.154 | 3.021 | 2.749 | 2.722 | 4.121 |

| No Default: Assets | 70.8 | 82.8 | 153.6 | 137.7 | 70.8 | 140.7 | 126.2 |

| With Default: Loss | 50 | 50 | 100 | 100 | 50 | 99.1 | 99.1 |

| With Default: Margin | 1.888 | 2.982 | 4.869 | 3.423 | 1.888 | 3.779 | 2.464 |

| With Default: Premium | 51.9 | 53 | 104.9 | 103.4 | 51.9 | 102.9 | 101.5 |

| With Default: Loss Ratio | 0.964 | 0.944 | 0.954 | 0.967 | 0.964 | 0.963 | 0.976 |

| With Default: Capital | 18.9 | 29.8 | 48.7 | 34.2 | 18.9 | 37.8 | 24.6 |

| With Default: Rate of Return | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| With Default: Leverage | 2.749 | 1.777 | 2.154 | 3.021 | 2.749 | 2.722 | 4.121 |

| With Default: Assets | 70.8 | 82.8 | 153.6 | 137.7 | 70.8 | 140.7 | 126.2 |

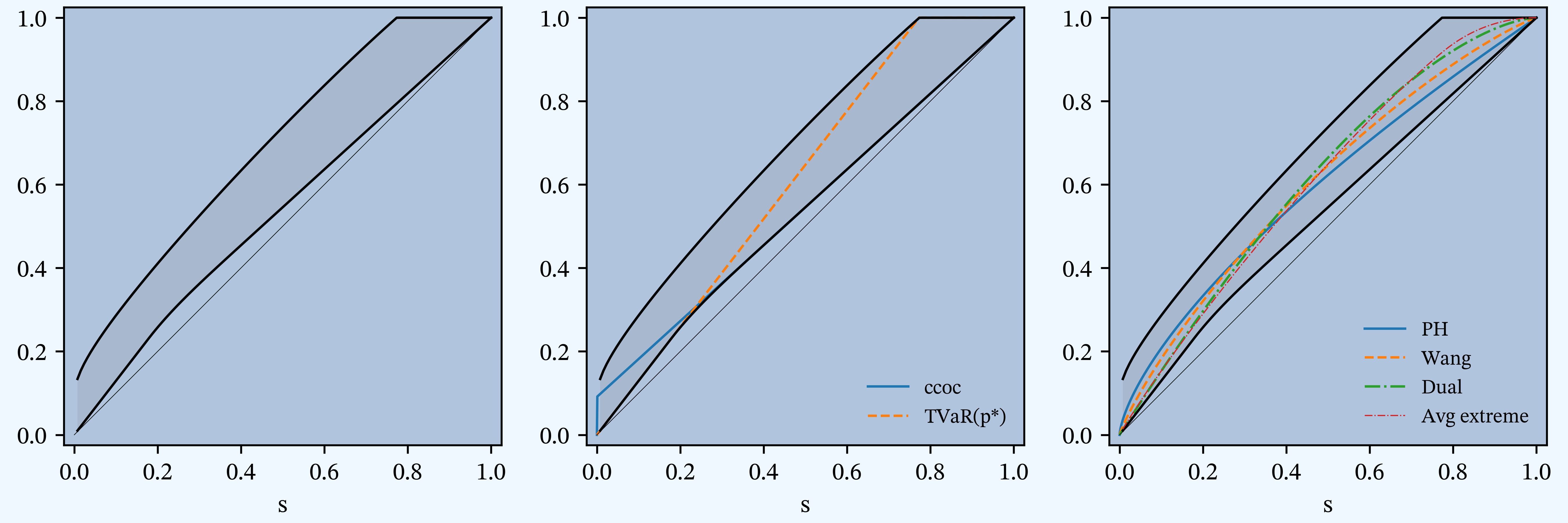

Figure M

PIR Chapter 11, Figures 11.2, 11.3, 11.4,11.5, Distortion envelope for Case Study, gross.

Table N

PIR Chapter 11, Table 11.5, Parameters for the six SRMs and associated distortions.

| method | Param | Error | Premium | K | Ι | S |

|---|---|---|---|---|---|---|

| Ccoc | 0.1 | 0 | 103.423 | 34.233 | 0.1 | 9.9957e-05 |

| PH | 0.683 | 0 | 103.423 | 34.233 | 0.1 | 9.9957e-05 |

| Wang | 0.375 | 0 | 103.423 | 34.233 | 0.1 | 9.9957e-05 |

| Dual | 1.576 | -0 | 103.423 | 34.233 | 0.1 | 9.9957e-05 |

| Tvar | 0.227 | 0 | 103.423 | 34.233 | 0.1 | 9.9957e-05 |

Figure O

PIR Chapter 11, Figures 11.6, 11.7, 11.8, Variation in insurance statistics for six distortions as \(s\) varies.

Figure P

PIR Chapter 11, Figures 11.9, 11.10, 11.11, Variation in insurance statistics as the asset limit is varied.

Table Q

PIR Chapter 11, Tables 11.7, 11.8, 11.9, Pricing by unit and distortion for Case Study.

| Gross: A | Gross: B | Gross: SoP | Gross: Total | Net: B | Net: SoP | Net: Total | |

|---|---|---|---|---|---|---|---|

| Loss: Ccoc | 50 | 50 | 100 | 100 | 49.084 | 99.084 | 99.084 |

| Margin: Ccoc | 1.888 | 2.982 | 4.869 | 3.423 | 1.891 | 3.779 | 2.464 |

| Margin: PH | 1.896 | 2.891 | 4.787 | 3.423 | 1.822 | 3.718 | 2.765 |

| Margin: Wang | 1.898 | 2.861 | 4.759 | 3.423 | 2.09 | 3.988 | 2.904 |

| Margin: Dual | 1.9 | 2.835 | 4.735 | 3.423 | 2.355 | 4.255 | 3.03 |

| Margin: TVaR | 1.901 | 2.81 | 4.711 | 3.423 | 2.541 | 4.442 | 3.155 |

| Margin: Blend | 1.898 | 2.853 | 4.752 | 3.423 | 2.193 | 4.091 | 2.956 |

| Premium: Ccoc | 51.888 | 52.981 | 104.869 | 103.423 | 50.976 | 102.863 | 101.548 |

| Premium: PH | 51.896 | 52.891 | 104.787 | 103.423 | 50.906 | 102.802 | 101.849 |

| Premium: Wang | 51.898 | 52.861 | 104.759 | 103.423 | 51.174 | 103.072 | 101.988 |

| Premium: Dual | 51.9 | 52.835 | 104.734 | 103.423 | 51.44 | 103.339 | 102.114 |

| Premium: TVaR | 51.901 | 52.81 | 104.711 | 103.423 | 51.625 | 103.526 | 102.239 |

| Premium: Blend | 51.898 | 52.853 | 104.751 | 103.423 | 51.277 | 103.175 | 102.04 |

| Loss Ratio: Ccoc | 0.964 | 0.944 | 0.954 | 0.967 | 0.963 | 0.963 | 0.976 |

| Loss Ratio: PH | 0.963 | 0.945 | 0.954 | 0.967 | 0.964 | 0.964 | 0.973 |

| Loss Ratio: Wang | 0.963 | 0.946 | 0.955 | 0.967 | 0.959 | 0.961 | 0.972 |

| Loss Ratio: Dual | 0.963 | 0.946 | 0.955 | 0.967 | 0.954 | 0.959 | 0.97 |

| Loss Ratio: TVaR | 0.963 | 0.947 | 0.955 | 0.967 | 0.951 | 0.957 | 0.969 |

| Loss Ratio: Blend | 0.963 | 0.946 | 0.955 | 0.967 | 0.957 | 0.96 | 0.971 |

| Capital: Ccoc | 18.878 | 29.816 | 48.694 | 34.233 | 18.915 | 37.793 | 24.639 |

| Capital: PH | 18.869 | 29.906 | 48.776 | 34.233 | 18.985 | 37.854 | 24.339 |

| Capital: Wang | 18.868 | 29.936 | 48.804 | 34.233 | 18.717 | 37.584 | 24.2 |

| Capital: Dual | 18.866 | 29.962 | 48.828 | 34.233 | 18.451 | 37.317 | 24.073 |

| Capital: TVaR | 18.865 | 29.987 | 48.852 | 34.233 | 18.265 | 37.13 | 23.949 |

| Capital: Blend | 18.868 | 29.944 | 48.811 | 34.233 | 18.613 | 37.481 | 24.148 |

| Rate of Return: Ccoc | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: PH | 0.1 | 0.097 | 0.098 | 0.1 | 0.096 | 0.098 | 0.114 |

| Rate of Return: Wang | 0.101 | 0.096 | 0.098 | 0.1 | 0.112 | 0.106 | 0.12 |

| Rate of Return: Dual | 0.101 | 0.095 | 0.097 | 0.1 | 0.128 | 0.114 | 0.126 |

| Rate of Return: TVaR | 0.101 | 0.094 | 0.096 | 0.1 | 0.139 | 0.12 | 0.132 |

| Rate of Return: Blend | 0.101 | 0.095 | 0.097 | 0.1 | 0.118 | 0.109 | 0.122 |

| Leverage: Ccoc | 2.749 | 1.777 | 2.154 | 3.021 | 2.695 | 2.722 | 4.121 |

| Leverage: PH | 2.75 | 1.769 | 2.148 | 3.021 | 2.681 | 2.716 | 4.185 |

| Leverage: Wang | 2.751 | 1.766 | 2.147 | 3.021 | 2.734 | 2.742 | 4.214 |

| Leverage: Dual | 2.751 | 1.763 | 2.145 | 3.021 | 2.788 | 2.769 | 4.242 |

| Leverage: TVaR | 2.751 | 1.761 | 2.143 | 3.021 | 2.826 | 2.788 | 4.269 |

| Leverage: Blend | 2.751 | 1.765 | 2.146 | 3.021 | 2.755 | 2.753 | 4.226 |

| Assets: Ccoc | 70.766 | 82.797 | 153.562 | 137.656 | 69.891 | 140.656 | 126.188 |

Table R

PIR Chapter 13, Table 13.1, Comparison of gross expected losses by Case, catastrophe-prone lines.

| Unit | a | E[Xi(a)] | E[Xi ∧ ai] |

|---|---|---|---|

| A | 70.766 | 50 | 50 |

| B | 82.797 | 50 | 50 |

| Total | 137.656 | 100 | 100 |

| SoP | 153.562 | 100 | 100 |

Table S

PIR Chapter 13, Tables 13.2, 13.3, 13.4, Constant 0.10 ROE pricing for Case Study, classical PCP methods.

| Gross: A | Gross: B | Gross: Total | Net: A | Net: B | Net: Total | Ceded: Diff | |

|---|---|---|---|---|---|---|---|

| Loss: Expected Loss | 50 | 50 | 100 | 50 | 49.084 | 99.084 | 0.916 |

| Margin: Expected Loss | 1.712 | 1.712 | 3.423 | 1.243 | 1.221 | 2.464 | 0.959 |

| Margin: Scaled EPD | nan | nan | nan | 1.16 | 1.304 | 2.464 | nan |

| Margin: Scaled TVaR | nan | nan | nan | 1.227 | 1.237 | 2.464 | nan |

| Margin: Scaled VaR | nan | nan | nan | 1.225 | 1.239 | 2.464 | nan |

| Margin: Equal Risk EPD | nan | nan | nan | 1.338 | 1.126 | 2.464 | nan |

| Margin: Equal Risk TVaR | nan | nan | nan | 1.389 | 1.075 | 2.464 | nan |

| Margin: Equal Risk VaR | nan | nan | nan | 1.391 | 1.075 | 2.464 | nan |

| Margin: coTVaR | nan | nan | nan | 1.39 | 1.075 | 2.465 | nan |

| Margin: Covar | nan | nan | nan | 1.003 | 1.461 | 2.464 | nan |

| Premium: Expected Loss | 51.712 | 51.711 | 103.423 | 51.243 | 50.305 | 101.548 | 1.875 |

| Premium: Scaled EPD | nan | nan | nan | 51.16 | 50.388 | 101.548 | nan |

| Premium: Scaled TVaR | nan | nan | nan | 51.227 | 50.321 | 101.548 | nan |

| Premium: Scaled VaR | nan | nan | nan | 51.225 | 50.323 | 101.548 | nan |

| Premium: Equal Risk EPD | nan | nan | nan | 51.338 | 50.21 | 101.548 | nan |

| Premium: Equal Risk TVaR | nan | nan | nan | 51.389 | 50.159 | 101.548 | nan |

| Premium: Equal Risk VaR | nan | nan | nan | 51.391 | 50.159 | 101.548 | nan |

| Premium: coTVaR | nan | nan | nan | 51.39 | 50.159 | 101.549 | nan |

| Premium: Covar | nan | nan | nan | 51.002 | 50.546 | 101.548 | nan |

| Loss Ratio: Expected Loss | 0.967 | 0.967 | 0.967 | 0.976 | 0.976 | 0.976 | 0.488 |

| Loss Ratio: Scaled EPD | nan | nan | nan | 0.977 | 0.974 | 0.976 | nan |

| Loss Ratio: Scaled TVaR | nan | nan | nan | 0.976 | 0.975 | 0.976 | nan |

| Loss Ratio: Scaled VaR | nan | nan | nan | 0.976 | 0.975 | 0.976 | nan |

| Loss Ratio: Equal Risk EPD | nan | nan | nan | 0.974 | 0.978 | 0.976 | nan |

| Loss Ratio: Equal Risk TVaR | nan | nan | nan | 0.973 | 0.979 | 0.976 | nan |

| Loss Ratio: Equal Risk VaR | nan | nan | nan | 0.973 | 0.979 | 0.976 | nan |

| Loss Ratio: coTVaR | nan | nan | nan | 0.973 | 0.979 | 0.976 | nan |

| Loss Ratio: Covar | nan | nan | nan | 0.98 | 0.971 | 0.976 | nan |

| Capital: Expected Loss | 17.117 | 17.117 | 34.233 | 12.434 | 12.206 | 24.639 | 9.594 |

| Capital: Scaled EPD | nan | nan | nan | 11.603 | 13.036 | 24.639 | nan |

| Capital: Scaled TVaR | nan | nan | nan | 12.271 | 12.368 | 24.639 | nan |

| Capital: Scaled VaR | nan | nan | nan | 12.254 | 12.385 | 24.639 | nan |

| Capital: Equal Risk EPD | nan | nan | nan | 13.379 | 11.261 | 24.639 | nan |

| Capital: Equal Risk TVaR | nan | nan | nan | 13.894 | 10.745 | 24.639 | nan |

| Capital: Equal Risk VaR | nan | nan | nan | 13.906 | 10.747 | 24.639 | nan |

| Capital: coTVaR | nan | nan | nan | 13.904 | 10.749 | 24.653 | nan |

| Capital: Covar | nan | nan | nan | 10.026 | 14.613 | 24.639 | nan |

| Rate of Return: Expected Loss | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: Scaled EPD | nan | nan | nan | 0.1 | 0.1 | 0.1 | nan |

| Rate of Return: Scaled TVaR | nan | nan | nan | 0.1 | 0.1 | 0.1 | nan |

| Rate of Return: Scaled VaR | nan | nan | nan | 0.1 | 0.1 | 0.1 | nan |

| Rate of Return: Equal Risk EPD | nan | nan | nan | 0.1 | 0.1 | 0.1 | nan |

| Rate of Return: Equal Risk TVaR | nan | nan | nan | 0.1 | 0.1 | 0.1 | nan |

| Rate of Return: Equal Risk VaR | nan | nan | nan | 0.1 | 0.1 | 0.1 | nan |

| Rate of Return: coTVaR | nan | nan | nan | 0.1 | 0.1 | 0.1 | nan |

| Rate of Return: Covar | nan | nan | nan | 0.1 | 0.1 | 0.1 | nan |

| Leverage: Expected Loss | 3.021 | 3.021 | 3.021 | 4.121 | 4.121 | 4.121 | 0.195 |

| Leverage: Scaled EPD | nan | nan | nan | 4.409 | 3.865 | 4.121 | nan |

| Leverage: Scaled TVaR | nan | nan | nan | 4.175 | 4.069 | 4.121 | nan |

| Leverage: Scaled VaR | nan | nan | nan | 4.18 | 4.063 | 4.121 | nan |

| Leverage: Equal Risk EPD | nan | nan | nan | 3.837 | 4.459 | 4.121 | nan |

| Leverage: Equal Risk TVaR | nan | nan | nan | 3.699 | 4.668 | 4.121 | nan |

| Leverage: Equal Risk VaR | nan | nan | nan | 3.695 | 4.667 | 4.121 | nan |

| Leverage: coTVaR | nan | nan | nan | 3.696 | 4.667 | 4.119 | nan |

| Leverage: Covar | nan | nan | nan | 5.087 | 3.459 | 4.121 | nan |

| Assets: Expected Loss | 68.828 | 68.828 | 137.656 | 63.677 | 62.511 | 126.188 | 11.469 |

| Assets: Scaled EPD | nan | nan | nan | 62.764 | 63.424 | 126.188 | nan |

| Assets: Scaled TVaR | nan | nan | nan | 63.498 | 62.689 | 126.188 | nan |

| Assets: Scaled VaR | nan | nan | nan | 63.479 | 62.708 | 126.188 | nan |

| Assets: Equal Risk EPD | nan | nan | nan | 64.716 | 61.471 | 126.188 | nan |

| Assets: Equal Risk TVaR | nan | nan | nan | 65.283 | 60.904 | 126.188 | nan |

| Assets: Equal Risk VaR | nan | nan | nan | 65.297 | 60.906 | 126.188 | nan |

| Assets: coTVaR | nan | nan | nan | 65.294 | 60.908 | 126.202 | nan |

| Assets: Covar | nan | nan | nan | 61.029 | 65.159 | 126.188 | nan |

Figure T_gross

Figure T_net

Figure U

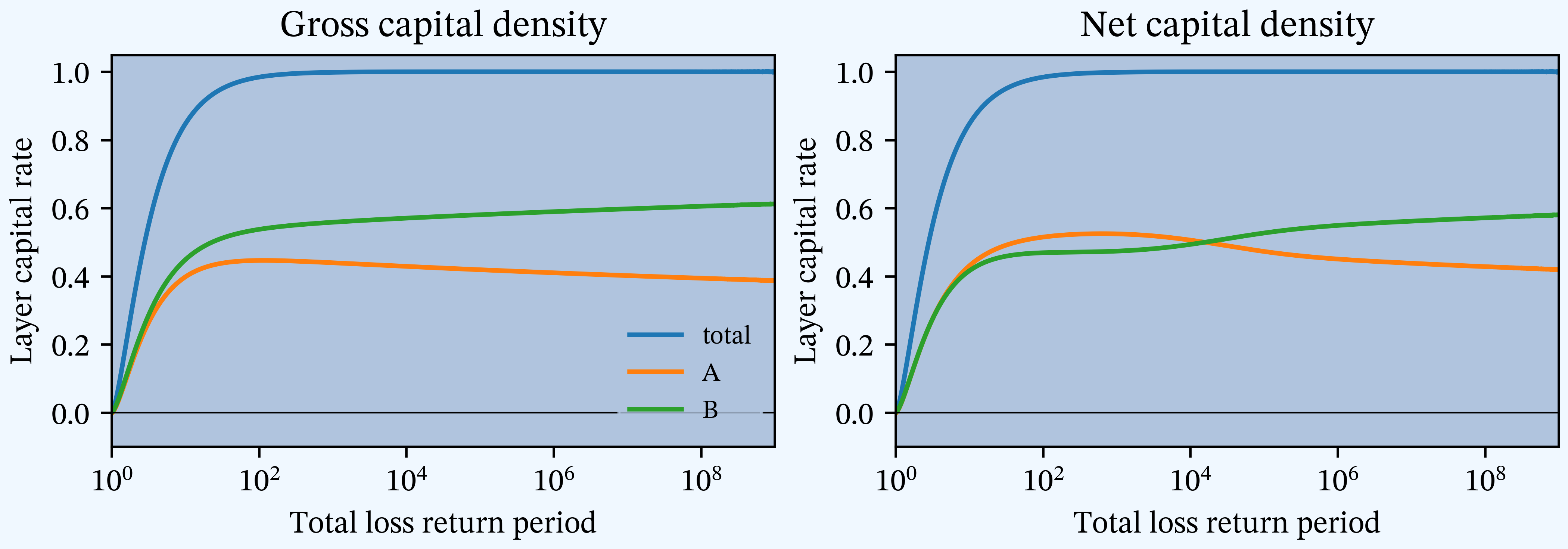

PIR Chapter 15, Figures 15.8, 15.9, 15.10, Capital density by layer.

Table V

PIR Chapter 15, Tables 15.35, 15.36, 15.37, Constant 0.10 ROE pricing for Cat/Non-Cat Case Study, distortion, SRM methods.

| Gross: A | Gross: B | Gross: Total | Net: A | Net: B | Net: Total | Ceded: Diff | |

|---|---|---|---|---|---|---|---|

| Loss: Expected Loss | 50 | 50 | 100 | 50 | 49.08 | 99.08 | 0.916 |

| Margin: Expected Loss | 1.712 | 1.712 | 3.423 | 1.243 | 1.221 | 2.464 | 0.959 |

| Margin: Dist Ccoc | 0.224 | 3.199 | 3.423 | 0.177 | 2.287 | 2.464 | 0.959 |

| Margin: Dist PH | 1 | 2.423 | 3.423 | 1.374 | 1.391 | 2.765 | 0.659 |

| Margin: Dist Wang | 1.038 | 2.386 | 3.423 | 1.276 | 1.627 | 2.904 | 0.52 |

| Margin: Dist Dual | 1.068 | 2.355 | 3.423 | 1.18 | 1.85 | 3.03 | 0.393 |

| Margin: Dist Tvar | 1.096 | 2.327 | 3.423 | 1.102 | 2.053 | 3.155 | 0.269 |

| Margin: Dist Blend | 1.045 | 2.378 | 3.423 | 1.237 | 1.718 | 2.956 | 0.468 |

| Premium: Expected Loss | 51.71 | 51.71 | 103.42 | 51.24 | 50.3 | 101.55 | 1.875 |

| Premium: Dist Ccoc | 50.22 | 53.2 | 103.42 | 50.18 | 51.37 | 101.55 | 1.875 |

| Premium: Dist PH | 51 | 52.42 | 103.42 | 51.37 | 50.48 | 101.85 | 1.574 |

| Premium: Dist Wang | 51.04 | 52.39 | 103.42 | 51.28 | 50.71 | 101.99 | 1.435 |

| Premium: Dist Dual | 51.07 | 52.35 | 103.42 | 51.18 | 50.93 | 102.11 | 1.309 |

| Premium: Dist Tvar | 51.1 | 52.33 | 103.42 | 51.1 | 51.14 | 102.24 | 1.184 |

| Premium: Dist Blend | 51.04 | 52.38 | 103.42 | 51.24 | 50.8 | 102.04 | 1.383 |

| Loss Ratio: Expected Loss | 0.967 | 0.967 | 0.967 | 0.976 | 0.976 | 0.976 | 0.488 |

| Loss Ratio: Dist Ccoc | 0.996 | 0.94 | 0.967 | 0.996 | 0.955 | 0.976 | 0.488 |

| Loss Ratio: Dist PH | 0.98 | 0.954 | 0.967 | 0.973 | 0.972 | 0.973 | 0.582 |

| Loss Ratio: Dist Wang | 0.98 | 0.954 | 0.967 | 0.975 | 0.968 | 0.972 | 0.638 |

| Loss Ratio: Dist Dual | 0.979 | 0.955 | 0.967 | 0.977 | 0.964 | 0.97 | 0.699 |

| Loss Ratio: Dist Tvar | 0.979 | 0.956 | 0.967 | 0.978 | 0.96 | 0.969 | 0.773 |

| Loss Ratio: Dist Blend | 0.98 | 0.955 | 0.967 | 0.976 | 0.966 | 0.971 | 0.662 |

| Capital: Expected Loss | 17.12 | 17.12 | 34.23 | 12.43 | 12.21 | 24.64 | 9.59 |

| Capital: Dist Ccoc | 6.24 | 27.99 | 34.23 | 4.882 | 19.76 | 24.64 | 9.59 |

| Capital: Dist PH | 14.4 | 19.83 | 34.23 | 12.48 | 11.86 | 24.34 | 9.89 |

| Capital: Dist Wang | 15.48 | 18.75 | 34.23 | 12.44 | 11.76 | 24.2 | 10.03 |

| Capital: Dist Dual | 15.63 | 18.6 | 34.23 | 12.37 | 11.7 | 24.07 | 10.16 |

| Capital: Dist Tvar | 15.66 | 18.57 | 34.23 | 12.31 | 11.64 | 23.95 | 10.28 |

| Capital: Dist Blend | 14.84 | 19.39 | 34.23 | 12.21 | 11.94 | 24.15 | 10.09 |

| Rate of Return: Expected Loss | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: Dist Ccoc | 0.036 | 0.114 | 0.1 | 0.036 | 0.116 | 0.1 | 0.1 |

| Rate of Return: Dist PH | 0.069 | 0.122 | 0.1 | 0.11 | 0.117 | 0.114 | 0.067 |

| Rate of Return: Dist Wang | 0.067 | 0.127 | 0.1 | 0.103 | 0.138 | 0.12 | 0.052 |

| Rate of Return: Dist Dual | 0.068 | 0.127 | 0.1 | 0.095 | 0.158 | 0.126 | 0.039 |

| Rate of Return: Dist Tvar | 0.07 | 0.125 | 0.1 | 0.089 | 0.176 | 0.132 | 0.026 |

| Rate of Return: Dist Blend | 0.07 | 0.123 | 0.1 | 0.101 | 0.144 | 0.122 | 0.046 |

| Leverage: Expected Loss | 3.021 | 3.021 | 3.021 | 4.121 | 4.121 | 4.121 | 0.195 |

| Leverage: Dist Ccoc | 8.05 | 1.901 | 3.021 | 10.28 | 2.6 | 4.121 | 0.195 |

| Leverage: Dist PH | 3.542 | 2.643 | 3.021 | 4.117 | 4.255 | 4.185 | 0.159 |

| Leverage: Dist Wang | 3.296 | 2.794 | 3.021 | 4.121 | 4.313 | 4.214 | 0.143 |

| Leverage: Dist Dual | 3.267 | 2.814 | 3.021 | 4.136 | 4.353 | 4.242 | 0.129 |

| Leverage: Dist Tvar | 3.263 | 2.817 | 3.021 | 4.15 | 4.395 | 4.269 | 0.115 |

| Leverage: Dist Blend | 3.439 | 2.701 | 3.021 | 4.198 | 4.254 | 4.226 | 0.137 |

| Assets: Expected Loss | 68.83 | 68.83 | 137.66 | 63.68 | 62.51 | 126.19 | 11.47 |

| Assets: Dist Ccoc | 56.47 | 81.19 | 137.66 | 55.06 | 71.13 | 126.19 | 11.47 |

| Assets: Dist PH | 65.4 | 72.26 | 137.66 | 63.85 | 62.34 | 126.19 | 11.47 |

| Assets: Dist Wang | 66.52 | 71.14 | 137.66 | 63.72 | 62.47 | 126.19 | 11.47 |

| Assets: Dist Dual | 66.7 | 70.96 | 137.66 | 63.55 | 62.63 | 126.19 | 11.47 |

| Assets: Dist Tvar | 66.76 | 70.9 | 137.66 | 63.41 | 62.77 | 126.19 | 11.47 |

| Assets: Dist Blend | 65.89 | 71.77 | 137.66 | 63.44 | 62.74 | 126.19 | 11.47 |

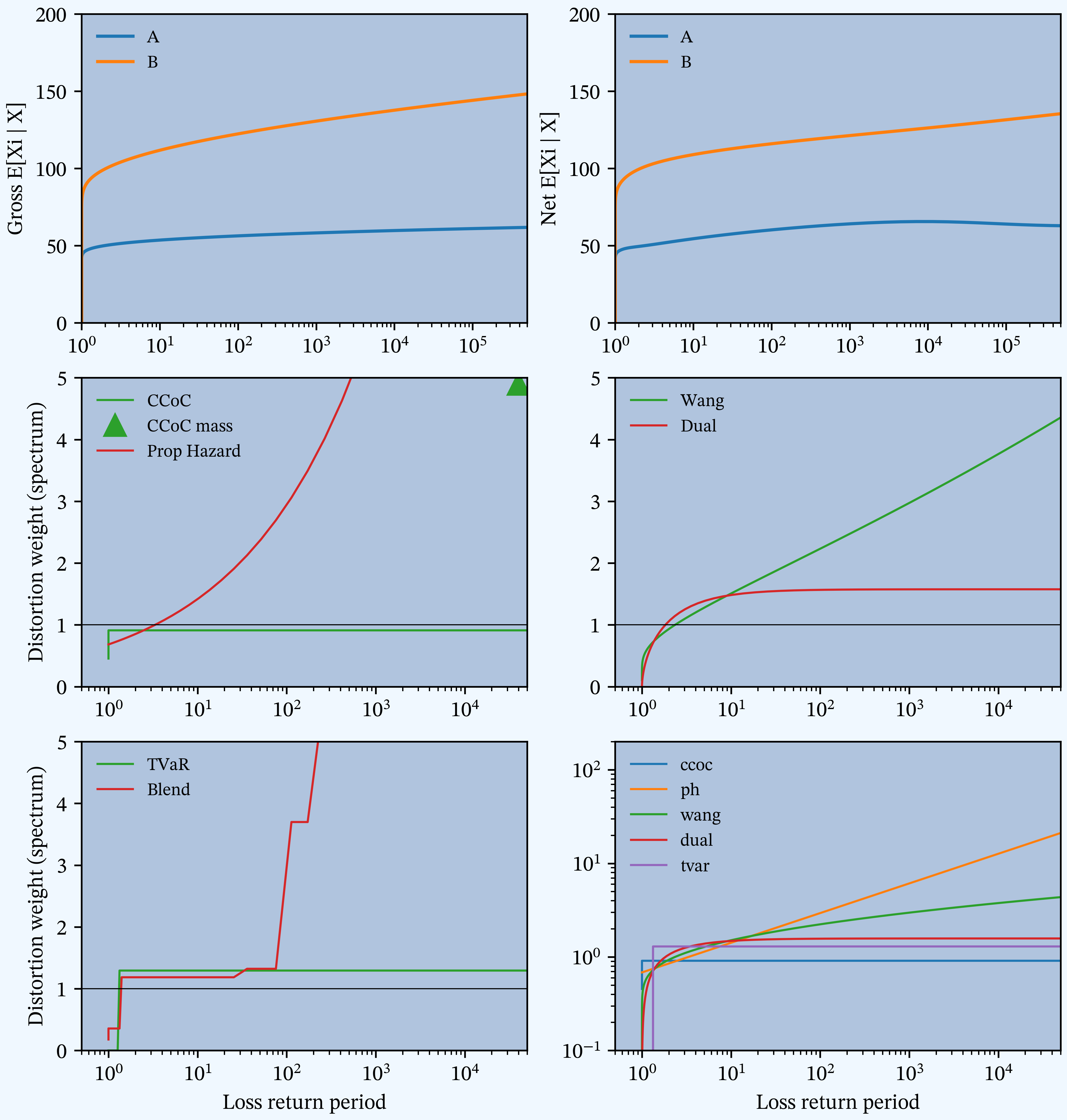

Figure W

PIR Chapter 15, Figure 15.11, Loss and loss spectrums.

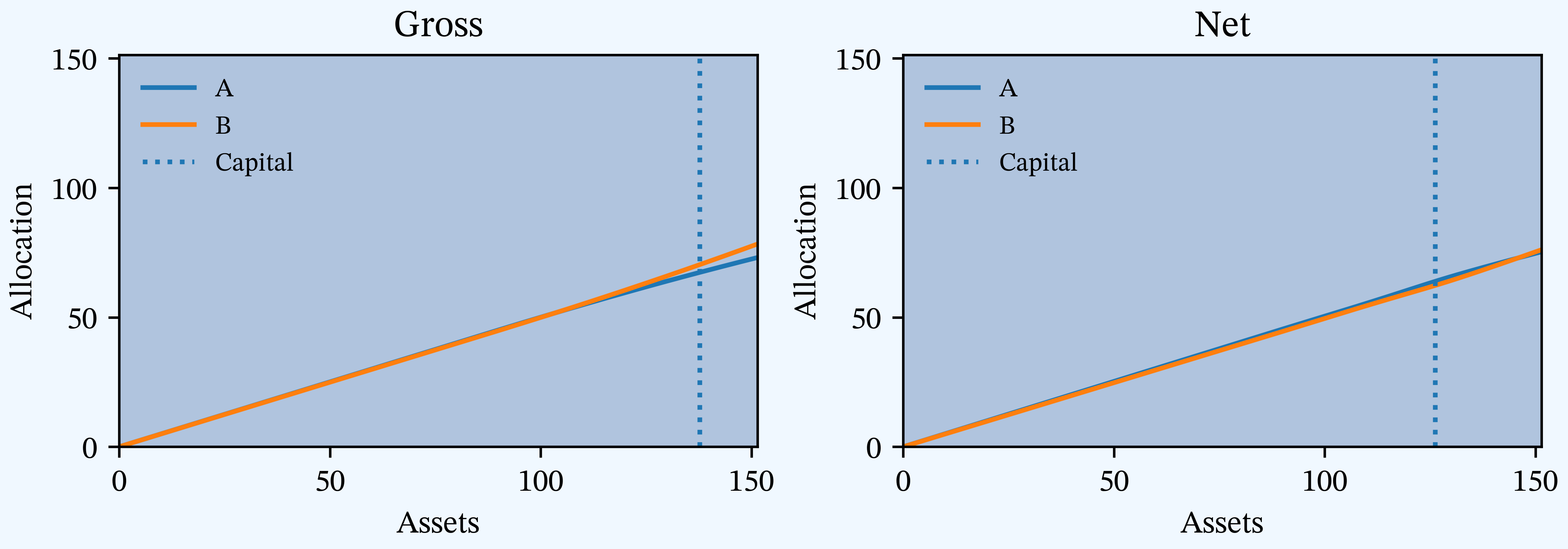

Figure X

PIR Chapter 15, Figures 15.12, 15.13, 15.14, Percentile layer of capital allocations by asset level.

Table Y

PIR Chapter 15, Tables 15.38, 15.39, 15.40, Percentile layer of capital allocations compared to distortion allocations.

| Method | Gross: A | Gross: B | Gross: Total | Net: A | Net: B | Net: Total | Ceded: Diff |

|---|---|---|---|---|---|---|---|

| Expected Loss | 68.83 | 68.83 | 137.7 | 63.68 | 62.51 | 126.2 | 11.47 |

| Dist Ccoc | 56.47 | 81.19 | 137.7 | 55.06 | 71.13 | 126.2 | 11.47 |

| Dist PH | 65.4 | 72.26 | 137.7 | 63.85 | 62.34 | 126.2 | 11.47 |

| Dist Wang | 66.52 | 71.14 | 137.7 | 63.72 | 62.47 | 126.2 | 11.47 |

| Dist Dual | 66.7 | 70.96 | 137.7 | 63.55 | 62.63 | 126.2 | 11.47 |

| Dist Tvar | 66.76 | 70.9 | 137.7 | 63.41 | 62.77 | 126.2 | 11.47 |

| Dist Blend | 65.89 | 71.77 | 137.7 | 63.44 | 62.74 | 126.2 | 11.47 |

| PLC | 67.34 | 70.32 | 137.7 | 63.89 | 62.3 | 126.2 | 11.47 |

Tame Case Description

Tame Case in the new syntax.

Distributions

# Line A (usually thinner tailed)

agg A 1 claim sev gamma 50 cv 0.10 fixed

# Line B Gross (usually thicker tailed)

agg B 1 claim sev gamma 50 cv 0.15 fixed

# Line B Net

agg B 1 claim sev gamma 50 cv 0.15 fixed aggregate net of 12.90625 xs 56.171875Other Parameters

reg_p = 0.9999roe = 0.1d2tc = 0.3s_values = [0.005, 0.01, 0.03]gs_values = [0.029126, 0.047619, 0.074074]f_discrete = Falselog2 = 16bs = 0.015625padding = 1

Description of Tables and Figures

| Ref. | Kind | Chapter | Number(s) | Description |

|---|---|---|---|---|

| A | Table | 2 | 2.3, 2.5, 2.6, 2.7 | Estimated mean, CV, skewness and kurtosis by line and in total, gross and net. |

| B | Figure | 2 | 2.2, 2.4, 2.6 | Gross and net densities on a linear and log scale. |

| C | Figure | 2 | 2.3, 2.5, 2.7 | Bivariate densities: gross and net with gross sample. |

| D | Figure | 4 | 4.9, 4.10, 4.11, 4.12 | TVaR, and VaR for unlimited and limited variables, gross and net. |

| E | Table | 4 | 4.6, 4.7, 4.8 | Estimated VaR, TVaR, and EPD by line and in total, gross, and net. |

| F | Table | 7 | 7.2 | Pricing summary. |

| G | Table | 7 | 7.3 | Details of reinsurance. |

| H | Table | 9 | 9.2, 9.5, 9.8 | Classical pricing by method. |

| I | Table | 9 | 9.3, 9.6, 9.9 | Sum of parts (SoP) stand-alone vs. diversified classical pricing by method. |

| J | Table | 9 | 9.4, 9.7, 9.10 | Implied loss ratios from classical pricing by method. |

| K | Table | 9 | 9.11 | Comparison of stand-alone and sum of parts premium. |

| L | Table | 9 | 9.12, 9.13, 9.14 | Constant CoC pricing by unit for Case Study. |

| M | Figure | 11 | 11.2, 11.3, 11.4,11.5 | Distortion envelope for Case Study, gross. |

| N | Table | 11 | 11.5 | Parameters for the six SRMs and associated distortions. |

| O | Figure | 11 | 11.6, 11.7, 11.8 | Variation in insurance statistics for six distortions as \(s\) varies. |

| P | Figure | 11 | 11.9, 11.10, 11.11 | Variation in insurance statistics as the asset limit is varied. |

| Q | Table | 11 | 11.7, 11.8, 11.9 | Pricing by unit and distortion for Case Study. |

| R | Table | 13 | 13.1 missing | Comparison of gross expected losses by Case, catastrophe-prone lines. |

| S | Table | 13 | 13.2, 13.3, 13.4 | Constant 0.10 ROE pricing for Case Study, classical PCP methods. |

| T | Figure | 15 | 15.2 - 15.7 (G/N) | Twelve plot. |

| U | Figure | 15 | 15.8, 15.9, 15.10 | Capital density by layer. |

| V | Table | 15 | 15.35, 15.36, 15.37 | Constant 0.10 ROE pricing for Cat/Non-Cat Case Study, distortion, SRM methods. |

| W | Figure | 15 | 15.11 | Loss and loss spectrums. |

| X | Figure | 15 | 15.12, 15.13, 15.14 | Percentile layer of capital allocations by asset level. |

| Y | Table | 15 | 15.38, 15.39, 15.40 | Percentile layer of capital allocations compared to distortion allocations. |