Cat/Non-Cat Case Study PIR Exhibits

Cat/Non-Cat Book Case Study Results

Exhibits by Chapter

- Chapter 2: Basic loss statistics (A-C)

- Chapter 4: VaR, TVaR and EPD statistics (D, E)

- Chapter 7: Portfolio pricing, used for calibration (F, G)

- Chapter 9: Classical portfolio and stand-alone pricing (H-L)

- Chapter 11: Modern portfolio and stand-alone pricing (M-Q)

- Chapter 13: Classical allocations (R, S)

- Chapter 15: Modern allocations (T-Y)

See Section 1.28 for more details.

Table A

PIR Chapter 2, Tables 2.3, 2.5, 2.6, 2.7, Estimated mean, CV, skewness and kurtosis by line and in total, gross and net.

| statistic | Gross: Cat | Gross: NonCat | Gross: Total | Net: Cat | Net: NonCat | Net: Total |

|---|---|---|---|---|---|---|

| Mean | 20 | 80 | 100 | 17.786 | 80 | 97.786 |

| CV | 1 | 0.15 | 0.233 | 0.737 | 0.15 | 0.182 |

| Skewness | 3.972 | 0.3 | 2.539 | 3.139 | 0.3 | 1.351 |

| Kurtosis | 35.933 | 0.135 | 19.173 | 55.22 | 0.135 | 16.336 |

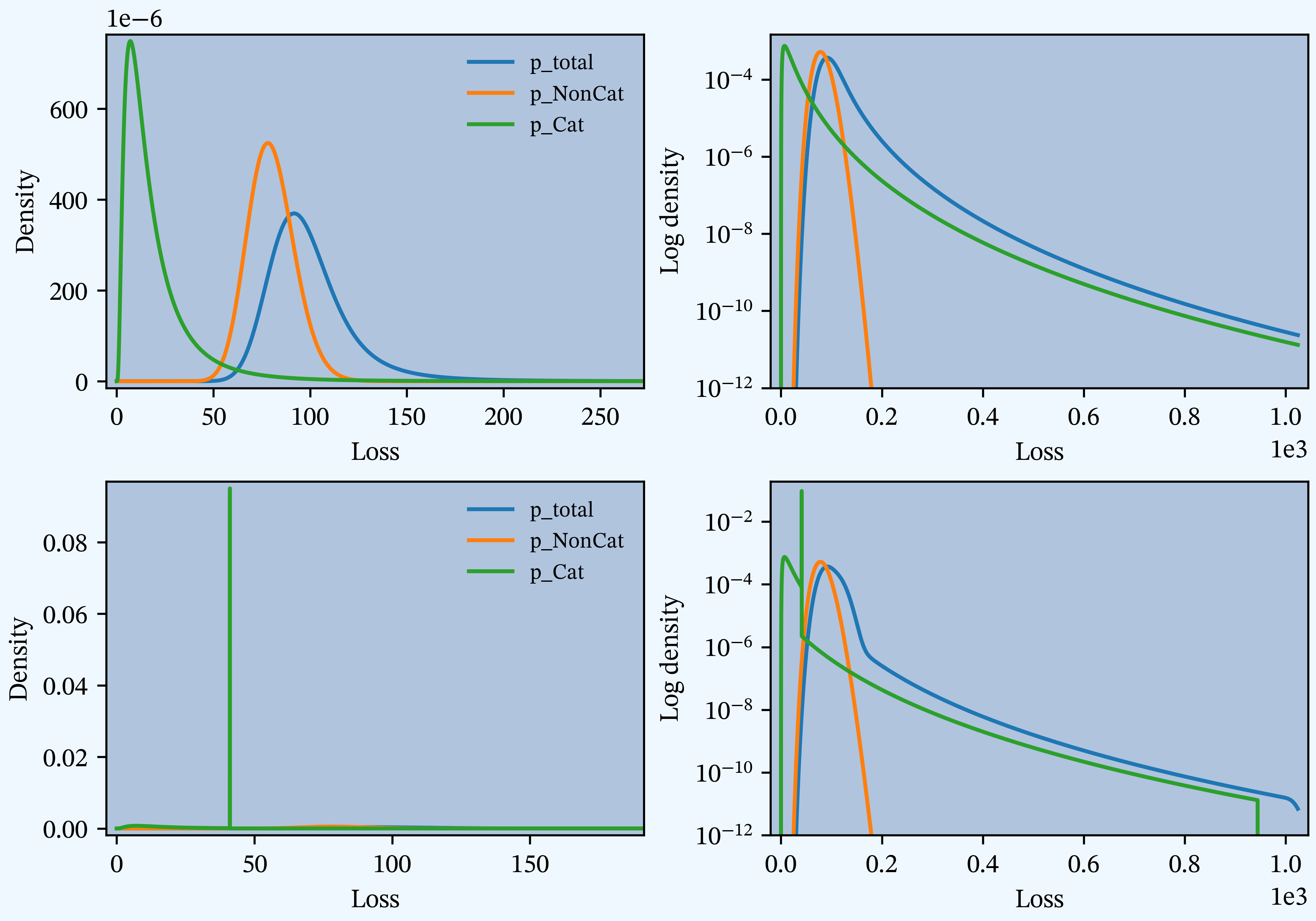

Figure B

PIR Chapter 2, Figures 2.2, 2.4, 2.6, Gross and net densities on a linear and log scale.

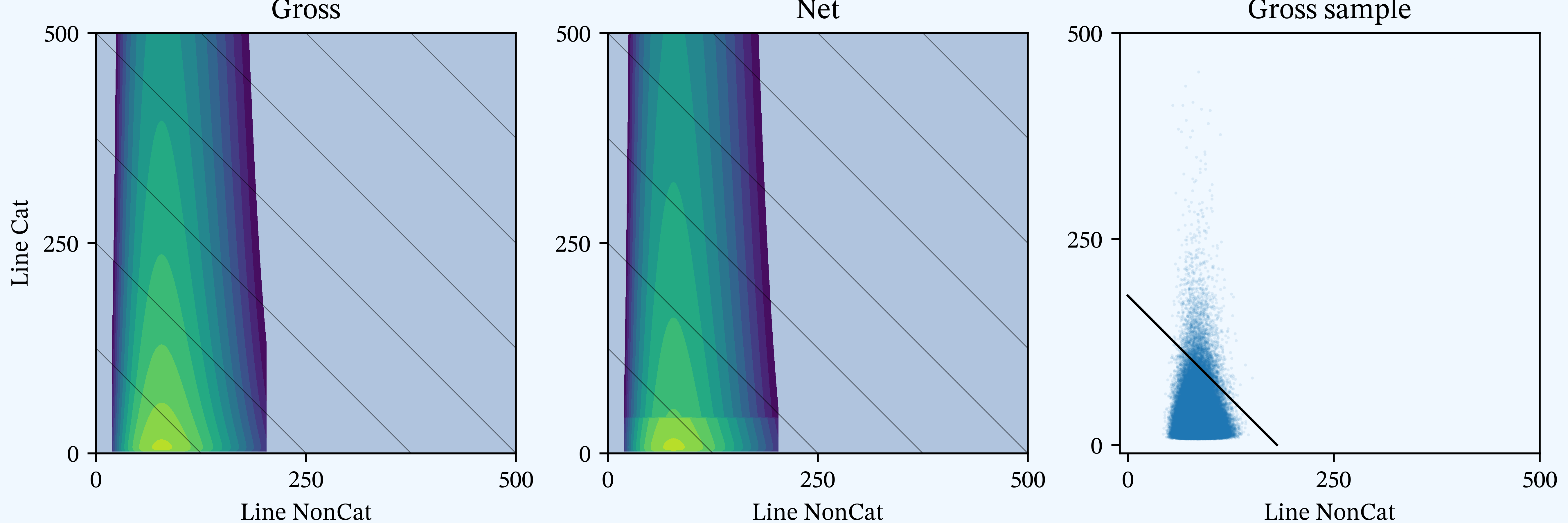

Figure C

PIR Chapter 2, Figures 2.3, 2.5, 2.7, Bivariate densities: gross and net with gross sample.

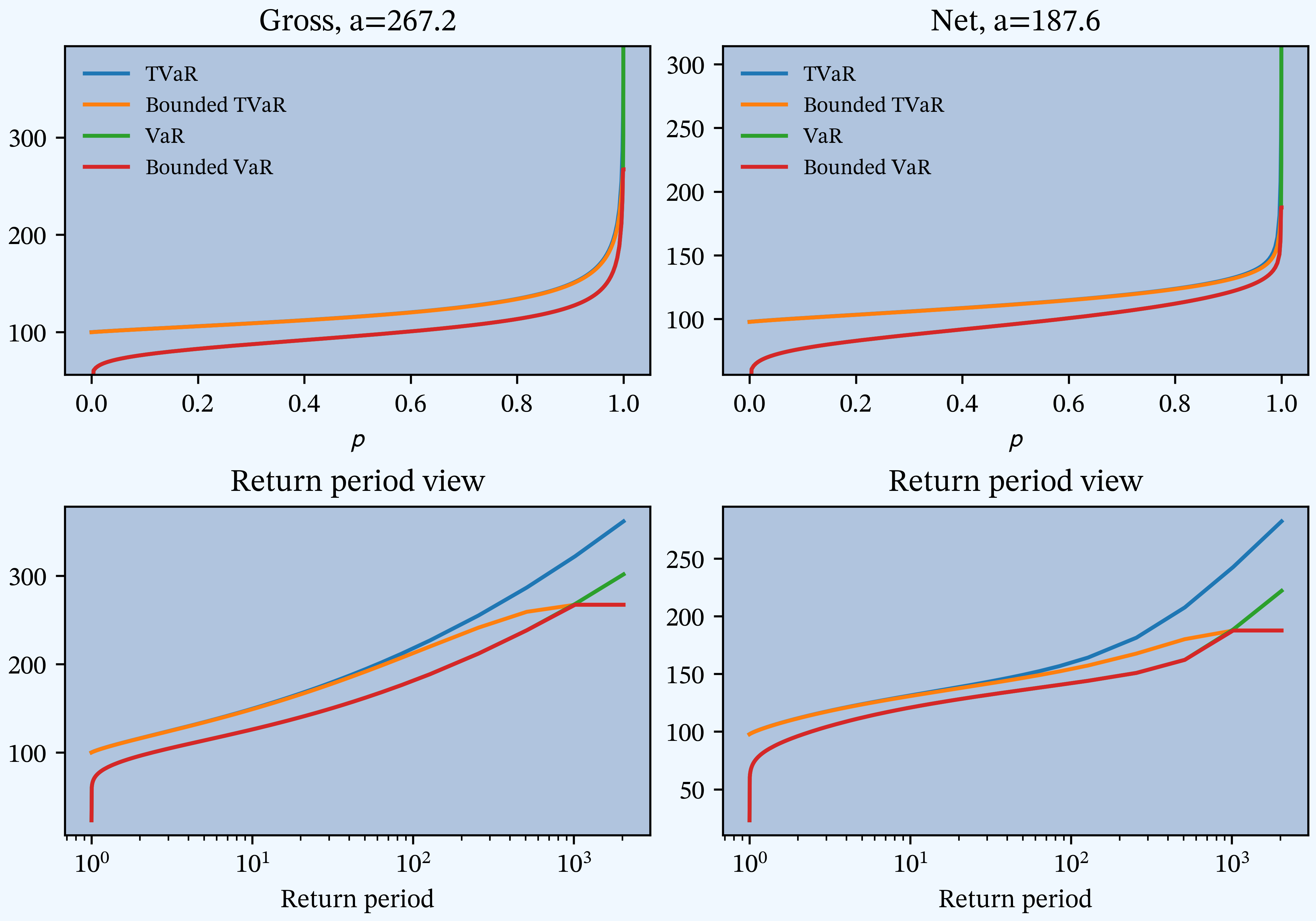

Figure D

PIR Chapter 4, Figures 4.9, 4.10, 4.11, 4.12, TVaR, and VaR for unlimited and limited variables, gross and net.

Table E

PIR Chapter 4, Tables 4.6, 4.7, 4.8, Estimated VaR, TVaR, and EPD by line and in total, gross, and net.

| statistic | Gross: Cat | Gross: NonCat | Gross: Benefit | Gross: Sum | Gross: Total | Net: Cat | Net: NonCat | Net: Benefit | Net: Sum | Net: Total |

|---|---|---|---|---|---|---|---|---|---|---|

| VaR 90.0 | 41.1 | 95.7 | 0.0857 | 136.8 | 126 | 41.1 | 95.7 | 0.132 | 136.8 | 120.8 |

| VaR 95.0 | 55.6 | 100.7 | 0.117 | 156.3 | 139.9 | 41.1 | 100.7 | 0.108 | 141.8 | 128 |

| VaR 97.5 | 72.3 | 105.2 | 0.138 | 177.5 | 156 | 41.1 | 105.2 | 0.0901 | 146.3 | 134.2 |

| VaR 99.0 | 98.1 | 110.5 | 0.152 | 208.6 | 181.1 | 41.1 | 110.5 | 0.0686 | 151.6 | 141.9 |

| VaR 99.6 | 128.7 | 115.4 | 0.156 | 244.1 | 211.1 | 49 | 115.4 | 0.0919 | 164.5 | 150.6 |

| VaR 99.9 | 185.3 | 122.2 | 0.151 | 307.5 | 267.2 | 105.6 | 122.2 | 0.215 | 227.9 | 187.6 |

| TVaR 90.0 | 65.3 | 102.4 | 0.122 | 167.7 | 149.4 | 43.2 | 102.4 | 0.108 | 145.6 | 131.3 |

| TVaR 95.0 | 83.3 | 106.7 | 0.139 | 190.1 | 166.8 | 45.3 | 106.7 | 0.0974 | 152 | 138.5 |

| TVaR 97.5 | 103.8 | 110.8 | 0.149 | 214.6 | 186.8 | 49.5 | 110.8 | 0.0953 | 160.2 | 146.3 |

| TVaR 99.0 | 135.2 | 115.7 | 0.153 | 250.9 | 217.7 | 62 | 115.7 | 0.114 | 177.7 | 159.5 |

| TVaR 99.6 | 172 | 120.3 | 0.15 | 292.3 | 254.1 | 92.4 | 120.3 | 0.177 | 212.7 | 180.8 |

| TVaR 99.9 | 239.5 | 126.7 | 0.141 | 366.3 | 321.1 | 159.9 | 126.7 | 0.187 | 286.6 | 241.5 |

| EPD 10.0 | 45.9 | 74.4 | 0.253 | 120.3 | 96 | 29.7 | 74.4 | 0.128 | 104.1 | 92.3 |

| EPD 5.0 | 65 | 81.7 | 0.338 | 146.7 | 109.7 | 35.3 | 81.7 | 0.139 | 117 | 102.7 |

| EPD 2.5 | 87.4 | 87.7 | 0.407 | 175.1 | 124.5 | 38.9 | 87.7 | 0.135 | 126.6 | 111.5 |

| EPD 1.0 | 122.6 | 94.5 | 0.464 | 217.1 | 148.2 | 48 | 94.5 | 0.172 | 142.4 | 121.6 |

| EPD 0.4 | 164.9 | 100.4 | 0.492 | 265.3 | 177.9 | 91.3 | 100.4 | 0.46 | 191.7 | 131.2 |

| EPD 0.1 | 244.5 | 108.2 | 0.496 | 352.8 | 235.7 | 172.6 | 108.2 | 0.776 | 280.8 | 158.1 |

Table F

PIR Chapter 7, Table 7.2, Pricing summary.

| stat | Gross | Net |

|---|---|---|

| Loss | 99.946 | 97.732 |

| Margin | 15.205 | 8.168 |

| Premium | 115.151 | 105.899 |

| Loss Ratio | 0.868 | 0.923 |

| Capital | 152.052 | 81.679 |

| Rate of Return | 0.1 | 0.1 |

| Assets | 267.203 | 187.578 |

| Leverage | 0.757 | 1.297 |

Table H

PIR Chapter 9, Tables 9.2, 9.5, 9.8, Classical pricing by method.

| method | Parameters: Value | Cat: Net | Cat: Gross | NonCat: Gross | Total: Net | Total: Gross | Total: Ceded |

|---|---|---|---|---|---|---|---|

| Net | 17.8 | 20 | 80 | 97.8 | 100 | 2.214 | |

| Expected Value | 0.152 | 20.5 | 23 | 92.1 | 112.6 | 115.2 | 2.55 |

| VaR | 0.818 | 30.1 | 30.1 | 90.7 | 113.4 | 115.1 | 1.75 |

| Variance | 0.028 | 22.6 | 31.1 | 84 | 106.6 | 115.2 | 8.6 |

| Dutch | 1.859 | 27.2 | 32 | 88.9 | 110.6 | 115.2 | 4.513 |

| Semi-Variance | 0.040 | 22.5 | 32.8 | 83.1 | 105.2 | 115.2 | 10 |

| Standard Deviation | 0.650 | 26.3 | 33 | 87.8 | 109.3 | 115.2 | 5.8 |

| Fischer | 0.776 | 26.2 | 33.9 | 86.8 | 108.4 | 115.2 | 6.8 |

| Esscher | 0.011 | 23.6 | 35.9 | 81.6 | 105.1 | 115.2 | 10.1 |

| Exponential | 0.014 | 24.8 | 39.7 | 81.1 | 105.6 | 115.2 | 9.5 |

Table I

PIR Chapter 9, Tables 9.3, 9.6, 9.9, Sum of parts (SoP) stand-alone vs. diversified classical pricing by method.

| method | Total: Gross | Total: Net | SoP: Gross | SoP: Net | Delta: Gross | Delta: Net |

|---|---|---|---|---|---|---|

| Net | 100 | 97.8 | 100 | 97.8 | 0 | 0 |

| Expected Value | 115.2 | 112.6 | 115.2 | 112.6 | 0 | 0 |

| VaR | 115.1 | 113.4 | 120.8 | 120.8 | 5.7 | 7.5 |

| Variance | 115.2 | 106.6 | 115.2 | 106.6 | 0.002 | 0 |

| Dutch | 115.2 | 110.6 | 120.9 | 116.1 | 5.7 | 5.4 |

| Semi-Variance | 115.2 | 105.2 | 115.9 | 105.6 | 0.726 | 0.41 |

| Standard Deviation | 115.2 | 109.3 | 120.8 | 114.1 | 5.6 | 4.767 |

| Fischer | 115.2 | 108.4 | 120.8 | 113.1 | 5.6 | 4.712 |

| Esscher | 115.2 | 105.1 | 117.5 | 105.1 | 2.354 | 0.083 |

| Exponential | 115.2 | 105.6 | 120.8 | 105.8 | 5.6 | 0.2 |

Table J

PIR Chapter 9, Tables 9.4, 9.7, 9.10, Implied loss ratios from classical pricing by method.

| method | Cat: Net | Cat: Gross | NonCat: Gross | Total: Net | Total: Gross | Total: Ceded |

|---|---|---|---|---|---|---|

| Net | 1 | 1 | 1 | 1 | 1 | 1 |

| Expected Value | 0.868 | 0.868 | 0.868 | 0.868 | 0.868 | 0.868 |

| VaR | 0.591 | 0.664 | 0.882 | 0.862 | 0.869 | 1.265 |

| Variance | 0.788 | 0.642 | 0.952 | 0.917 | 0.868 | 0.258 |

| Dutch | 0.655 | 0.625 | 0.9 | 0.884 | 0.868 | 0.491 |

| Semi-Variance | 0.79 | 0.61 | 0.963 | 0.93 | 0.868 | 0.222 |

| Standard Deviation | 0.676 | 0.606 | 0.911 | 0.894 | 0.868 | 0.381 |

| Fischer | 0.678 | 0.59 | 0.921 | 0.902 | 0.868 | 0.327 |

| Esscher | 0.754 | 0.556 | 0.981 | 0.931 | 0.868 | 0.219 |

| Exponential | 0.718 | 0.504 | 0.987 | 0.926 | 0.868 | 0.232 |

Table K

PIR Chapter 9, Table 9.11, Comparison of stand-alone and sum of parts premium.

| Gross SoP | Gross Total | Gross Redn | Net SoP | Net Total | Net Redn | |

|---|---|---|---|---|---|---|

| No Default: Loss | 100 | 100 | -0.0% | 97.8 | 97.8 | -0.0% |

| No Default: Premium | 118.9 | 115.2 | -3.1% | 109.6 | 105.9 | -3.3% |

| No Default: Capital | 188.7 | 152 | -19.4% | 118.3 | 81.6 | -31.0% |

| With Default: Loss | 99.9 | 99.9 | 0.0% | 97.7 | 97.7 | 0.0% |

| With Default: Premium | 118.8 | 115.2 | -3.1% | 109.6 | 105.9 | -3.3% |

| With Default: Capital | 188.7 | 152.1 | -19.4% | 118.3 | 81.7 | -31.0% |

Table L

PIR Chapter 9, Tables 9.12, 9.13, 9.14, Constant CoC pricing by unit for Case Study.

| Gross: Cat | Gross: NonCat | Gross: SoP | Gross: Total | Net: Cat | Net: SoP | Net: Total | |

|---|---|---|---|---|---|---|---|

| No Default: Loss | 20 | 80 | 100 | 100 | 17.8 | 97.8 | 97.8 |

| No Default: Margin | 15 | 3.841 | 18.9 | 15.2 | 8 | 11.8 | 8.2 |

| No Default: Premium | 35 | 83.8 | 118.9 | 115.2 | 25.8 | 109.6 | 105.9 |

| No Default: Loss Ratio | 0.571 | 0.954 | 0.841 | 0.868 | 0.69 | 0.892 | 0.923 |

| No Default: Capital | 150.3 | 38.4 | 188.7 | 152 | 79.9 | 118.3 | 81.6 |

| No Default: Rate of Return | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| No Default: Leverage | 0.233 | 2.183 | 0.63 | 0.758 | 0.323 | 0.927 | 1.298 |

| No Default: Assets | 185.3 | 122.2 | 307.5 | 267.2 | 105.6 | 227.9 | 187.6 |

| With Default: Loss | 19.9 | 80 | 99.9 | 99.9 | 17.7 | 97.7 | 97.7 |

| With Default: Margin | 15 | 3.841 | 18.9 | 15.2 | 8 | 11.8 | 8.2 |

| With Default: Premium | 35 | 83.8 | 118.8 | 115.2 | 25.7 | 109.6 | 105.9 |

| With Default: Loss Ratio | 0.57 | 0.954 | 0.841 | 0.868 | 0.689 | 0.892 | 0.923 |

| With Default: Capital | 150.3 | 38.4 | 188.7 | 152.1 | 79.9 | 118.3 | 81.7 |

| With Default: Rate of Return | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| With Default: Leverage | 0.233 | 2.183 | 0.63 | 0.757 | 0.322 | 0.926 | 1.297 |

| With Default: Assets | 185.3 | 122.2 | 307.5 | 267.2 | 105.6 | 227.9 | 187.6 |

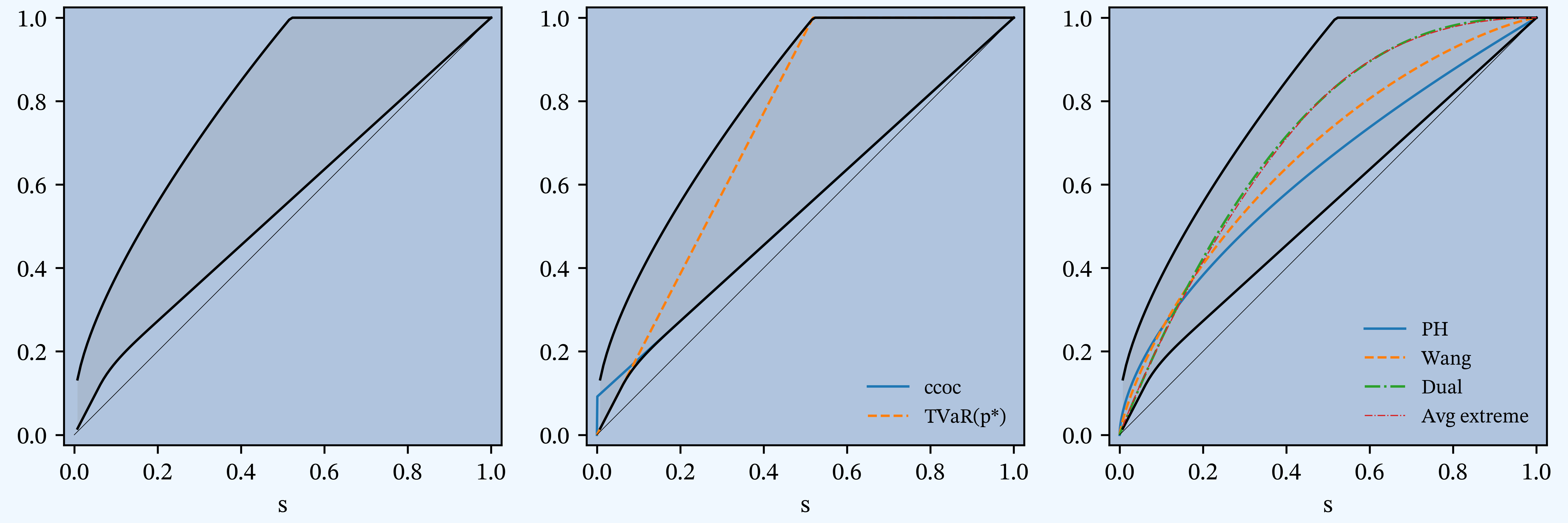

Figure M

PIR Chapter 11, Figures 11.2, 11.3, 11.4,11.5, Distortion envelope for Case Study, gross.

Table N

PIR Chapter 11, Table 11.5, Parameters for the six SRMs and associated distortions.

| method | Param | Error | Premium | K | Ι | S |

|---|---|---|---|---|---|---|

| Ccoc | 0.1 | 0 | 115.151 | 152.052 | 0.1 | 0.001 |

| PH | 0.596 | 0 | 115.151 | 152.052 | 0.1 | 0.001 |

| Wang | 0.611 | 0 | 115.151 | 152.052 | 0.1 | 0.001 |

| Dual | 2.463 | -0 | 115.151 | 152.052 | 0.1 | 0.001 |

| Tvar | 0.482 | 0 | 115.151 | 152.052 | 0.1 | 0.001 |

Figure O

PIR Chapter 11, Figures 11.6, 11.7, 11.8, Variation in insurance statistics for six distortions as \(s\) varies.

Figure P

PIR Chapter 11, Figures 11.9, 11.10, 11.11, Variation in insurance statistics as the asset limit is varied.

Table Q

PIR Chapter 11, Tables 11.7, 11.8, 11.9, Pricing by unit and distortion for Case Study.

| Gross: Cat | Gross: NonCat | Gross: SoP | Gross: Total | Net: Cat | Net: SoP | Net: Total | |

|---|---|---|---|---|---|---|---|

| Loss: Ccoc | 19.946 | 79.996 | 99.941 | 99.946 | 17.731 | 97.727 | 97.732 |

| Margin: Ccoc | 15.031 | 3.841 | 18.872 | 15.205 | 7.992 | 11.833 | 8.168 |

| Margin: PH | 13.806 | 6.367 | 20.172 | 15.205 | 7.379 | 13.746 | 9.821 |

| Margin: Wang | 12.876 | 7.507 | 20.383 | 15.205 | 7.947 | 15.454 | 11.058 |

| Margin: Dual | 11.882 | 8.598 | 20.481 | 15.205 | 8.834 | 17.433 | 12.402 |

| Margin: TVaR | 11.208 | 9.171 | 20.38 | 15.205 | 9.151 | 18.322 | 13.152 |

| Margin: Blend | 13.652 | 6.308 | 19.96 | 15.043 | 7.304 | 13.612 | 9.726 |

| Premium: Ccoc | 34.976 | 83.837 | 118.813 | 115.151 | 25.723 | 109.56 | 105.899 |

| Premium: PH | 33.751 | 86.362 | 120.113 | 115.151 | 25.11 | 111.472 | 107.553 |

| Premium: Wang | 32.821 | 87.502 | 120.324 | 115.151 | 25.679 | 113.181 | 108.79 |

| Premium: Dual | 31.828 | 88.594 | 120.422 | 115.151 | 26.566 | 115.16 | 110.134 |

| Premium: TVaR | 31.154 | 89.167 | 120.321 | 115.151 | 26.883 | 116.049 | 110.884 |

| Premium: Blend | 33.597 | 86.303 | 119.901 | 114.988 | 25.035 | 111.338 | 107.457 |

| Loss Ratio: Ccoc | 0.57 | 0.954 | 0.841 | 0.868 | 0.689 | 0.892 | 0.923 |

| Loss Ratio: PH | 0.591 | 0.926 | 0.832 | 0.868 | 0.706 | 0.877 | 0.909 |

| Loss Ratio: Wang | 0.608 | 0.914 | 0.831 | 0.868 | 0.691 | 0.863 | 0.898 |

| Loss Ratio: Dual | 0.627 | 0.903 | 0.83 | 0.868 | 0.667 | 0.849 | 0.887 |

| Loss Ratio: TVaR | 0.64 | 0.897 | 0.831 | 0.868 | 0.66 | 0.842 | 0.881 |

| Loss Ratio: Blend | 0.594 | 0.927 | 0.834 | 0.869 | 0.708 | 0.878 | 0.909 |

| Capital: Ccoc | 150.305 | 38.413 | 188.718 | 152.052 | 79.918 | 118.331 | 81.679 |

| Capital: PH | 151.53 | 35.888 | 187.418 | 152.052 | 80.53 | 116.418 | 80.025 |

| Capital: Wang | 152.46 | 34.748 | 187.207 | 152.052 | 79.962 | 114.709 | 78.788 |

| Capital: Dual | 153.454 | 33.656 | 187.11 | 152.052 | 79.075 | 112.731 | 77.445 |

| Capital: TVaR | 154.127 | 33.083 | 187.211 | 152.052 | 78.758 | 111.841 | 76.694 |

| Capital: Blend | 151.684 | 35.947 | 187.63 | 152.215 | 80.606 | 116.552 | 80.121 |

| Rate of Return: Ccoc | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: PH | 0.091 | 0.177 | 0.108 | 0.1 | 0.092 | 0.118 | 0.123 |

| Rate of Return: Wang | 0.084 | 0.216 | 0.109 | 0.1 | 0.099 | 0.135 | 0.14 |

| Rate of Return: Dual | 0.077 | 0.255 | 0.109 | 0.1 | 0.112 | 0.155 | 0.16 |

| Rate of Return: TVaR | 0.073 | 0.277 | 0.109 | 0.1 | 0.116 | 0.164 | 0.171 |

| Rate of Return: Blend | 0.09 | 0.175 | 0.106 | 0.099 | 0.091 | 0.117 | 0.121 |

| Leverage: Ccoc | 0.233 | 2.183 | 0.63 | 0.757 | 0.322 | 0.926 | 1.297 |

| Leverage: PH | 0.223 | 2.406 | 0.641 | 0.757 | 0.312 | 0.958 | 1.344 |

| Leverage: Wang | 0.215 | 2.518 | 0.643 | 0.757 | 0.321 | 0.987 | 1.381 |

| Leverage: Dual | 0.207 | 2.632 | 0.644 | 0.757 | 0.336 | 1.022 | 1.422 |

| Leverage: TVaR | 0.202 | 2.695 | 0.643 | 0.757 | 0.341 | 1.038 | 1.446 |

| Leverage: Blend | 0.221 | 2.401 | 0.639 | 0.755 | 0.311 | 0.955 | 1.341 |

| Assets: Ccoc | 185.281 | 122.25 | 307.531 | 267.203 | 105.641 | 227.891 | 187.578 |

Table R

PIR Chapter 13, Table 13.1, Comparison of gross expected losses by Case, catastrophe-prone lines.

| Unit | a | E[Xi(a)] | E[Xi ∧ ai] |

|---|---|---|---|

| NonCat | 122.25 | 79.988 | 79.996 |

| Cat | 185.281 | 19.958 | 19.946 |

| Total | 267.203 | 99.946 | 99.946 |

| SoP | 307.531 | 99.946 | 99.941 |

Table S

PIR Chapter 13, Tables 13.2, 13.3, 13.4, Constant 0.10 ROE pricing for Case Study, classical PCP methods.

| Gross: Cat | Gross: NonCat | Gross: Total | Net: Cat | Net: NonCat | Net: Total | Ceded: Diff | |

|---|---|---|---|---|---|---|---|

| Loss: Expected Loss | 19.958 | 79.988 | 99.946 | 17.747 | 79.985 | 97.732 | 2.214 |

| Margin: Expected Loss | 3.036 | 12.169 | 15.205 | 1.483 | 6.685 | 8.168 | 7.037 |

| Margin: Scaled EPD | 15.677 | -0.472 | 15.205 | 9.6 | -1.432 | 8.168 | 7.037 |

| Margin: Scaled TVaR | 12.846 | 2.36 | 15.205 | 6.166 | 2.002 | 8.168 | 7.037 |

| Margin: Scaled VaR | 12.82 | 2.385 | 15.205 | 6.292 | 1.876 | 8.168 | 7.037 |

| Margin: Equal Risk EPD | 13.335 | 1.87 | 15.205 | 6.355 | 1.813 | 8.168 | 7.037 |

| Margin: Equal Risk TVaR | 11.785 | 3.42 | 15.205 | 4.767 | 3.4 | 8.168 | 7.037 |

| Margin: Equal Risk VaR | 11.735 | 3.47 | 15.205 | 4.698 | 3.47 | 8.168 | 7.037 |

| Margin: coTVaR | 14.84 | 0.37 | 15.207 | 6.845 | 1.326 | 8.171 | 7.036 |

| Margin: Covar | 11.181 | 4.027 | 15.205 | 4.443 | 3.725 | 8.168 | 7.037 |

| Premium: Expected Loss | 22.994 | 92.157 | 115.151 | 19.23 | 86.669 | 105.899 | 9.252 |

| Premium: Scaled EPD | 35.635 | 79.516 | 115.151 | 27.347 | 78.552 | 105.899 | 9.252 |

| Premium: Scaled TVaR | 32.803 | 82.348 | 115.151 | 23.913 | 81.987 | 105.899 | 9.252 |

| Premium: Scaled VaR | 32.778 | 82.373 | 115.151 | 24.039 | 81.861 | 105.899 | 9.252 |

| Premium: Equal Risk EPD | 33.293 | 81.858 | 115.151 | 24.102 | 81.797 | 105.899 | 9.252 |

| Premium: Equal Risk TVaR | 31.743 | 83.408 | 115.151 | 22.515 | 83.385 | 105.899 | 9.252 |

| Premium: Equal Risk VaR | 31.693 | 83.458 | 115.151 | 22.445 | 83.455 | 105.899 | 9.252 |

| Premium: coTVaR | 34.798 | 80.358 | 115.153 | 24.592 | 81.311 | 105.902 | 9.25 |

| Premium: Covar | 31.138 | 84.015 | 115.151 | 22.19 | 83.709 | 105.899 | 9.252 |

| Loss Ratio: Expected Loss | 0.868 | 0.868 | 0.868 | 0.923 | 0.923 | 0.923 | 0.239 |

| Loss Ratio: Scaled EPD | 0.56 | 1.006 | 0.868 | 0.649 | 1.018 | 0.923 | 0.239 |

| Loss Ratio: Scaled TVaR | 0.608 | 0.971 | 0.868 | 0.742 | 0.976 | 0.923 | 0.239 |

| Loss Ratio: Scaled VaR | 0.609 | 0.971 | 0.868 | 0.738 | 0.977 | 0.923 | 0.239 |

| Loss Ratio: Equal Risk EPD | 0.599 | 0.977 | 0.868 | 0.736 | 0.978 | 0.923 | 0.239 |

| Loss Ratio: Equal Risk TVaR | 0.629 | 0.959 | 0.868 | 0.788 | 0.959 | 0.923 | 0.239 |

| Loss Ratio: Equal Risk VaR | 0.63 | 0.958 | 0.868 | 0.791 | 0.958 | 0.923 | 0.239 |

| Loss Ratio: coTVaR | 0.574 | 0.995 | 0.868 | 0.722 | 0.984 | 0.923 | 0.239 |

| Loss Ratio: Covar | 0.641 | 0.952 | 0.868 | 0.8 | 0.956 | 0.923 | 0.239 |

| Capital: Expected Loss | 30.363 | 121.689 | 152.052 | 14.832 | 66.847 | 81.679 | 70.373 |

| Capital: Scaled EPD | 156.767 | -4.715 | 152.052 | 96 | -14.321 | 81.679 | 70.373 |

| Capital: Scaled TVaR | 128.455 | 23.597 | 152.052 | 61.657 | 20.022 | 81.679 | 70.373 |

| Capital: Scaled VaR | 128.203 | 23.849 | 152.052 | 62.916 | 18.763 | 81.679 | 70.373 |

| Capital: Equal Risk EPD | 133.349 | 18.703 | 152.052 | 63.551 | 18.127 | 81.679 | 70.373 |

| Capital: Equal Risk TVaR | 117.848 | 34.205 | 152.052 | 47.674 | 34.004 | 81.679 | 70.373 |

| Capital: Equal Risk VaR | 117.354 | 34.698 | 152.052 | 46.977 | 34.702 | 81.679 | 70.373 |

| Capital: coTVaR | 148.399 | 3.698 | 152.067 | 68.445 | 13.262 | 81.706 | 70.361 |

| Capital: Covar | 111.806 | 40.27 | 152.052 | 44.433 | 37.246 | 81.679 | 70.373 |

| Rate of Return: Expected Loss | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: Scaled EPD | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: Scaled TVaR | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: Scaled VaR | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: Equal Risk EPD | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: Equal Risk TVaR | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: Equal Risk VaR | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: coTVaR | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: Covar | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Leverage: Expected Loss | 0.757 | 0.757 | 0.757 | 1.297 | 1.297 | 1.297 | 0.131 |

| Leverage: Scaled EPD | 0.227 | -16.863 | 0.757 | 0.285 | -5.485 | 1.297 | 0.131 |

| Leverage: Scaled TVaR | 0.255 | 3.49 | 0.757 | 0.388 | 4.095 | 1.297 | 0.131 |

| Leverage: Scaled VaR | 0.256 | 3.454 | 0.757 | 0.382 | 4.363 | 1.297 | 0.131 |

| Leverage: Equal Risk EPD | 0.25 | 4.377 | 0.757 | 0.379 | 4.512 | 1.297 | 0.131 |

| Leverage: Equal Risk TVaR | 0.269 | 2.439 | 0.757 | 0.472 | 2.452 | 1.297 | 0.131 |

| Leverage: Equal Risk VaR | 0.27 | 2.405 | 0.757 | 0.478 | 2.405 | 1.297 | 0.131 |

| Leverage: coTVaR | 0.234 | 21.728 | 0.757 | 0.359 | 6.131 | 1.296 | 0.131 |

| Leverage: Covar | 0.279 | 2.086 | 0.757 | 0.499 | 2.247 | 1.297 | 0.131 |

| Assets: Expected Loss | 53.357 | 213.846 | 267.203 | 34.062 | 153.516 | 187.578 | 79.625 |

| Assets: Scaled EPD | 192.402 | 74.801 | 267.203 | 123.347 | 64.231 | 187.578 | 79.625 |

| Assets: Scaled TVaR | 161.259 | 105.944 | 267.203 | 85.57 | 102.009 | 187.578 | 79.625 |

| Assets: Scaled VaR | 160.982 | 106.222 | 267.203 | 86.954 | 100.624 | 187.578 | 79.625 |

| Assets: Equal Risk EPD | 166.642 | 100.561 | 267.203 | 87.654 | 99.925 | 187.578 | 79.625 |

| Assets: Equal Risk TVaR | 149.59 | 117.613 | 267.203 | 70.189 | 117.389 | 187.578 | 79.625 |

| Assets: Equal Risk VaR | 149.047 | 118.156 | 267.203 | 69.422 | 118.156 | 187.578 | 79.625 |

| Assets: coTVaR | 183.197 | 84.056 | 267.22 | 93.037 | 94.573 | 187.608 | 79.612 |

| Assets: Covar | 142.944 | 124.285 | 267.203 | 66.624 | 120.956 | 187.578 | 79.625 |

Figure T_gross

Figure T_net

Figure U

PIR Chapter 15, Figures 15.8, 15.9, 15.10, Capital density by layer.

Table V

PIR Chapter 15, Tables 15.35, 15.36, 15.37, Constant 0.10 ROE pricing for Cat/Non-Cat Case Study, distortion, SRM methods.

| Gross: Cat | Gross: NonCat | Gross: Total | Net: Cat | Net: NonCat | Net: Total | Ceded: Diff | |

|---|---|---|---|---|---|---|---|

| Loss: Expected Loss | 19.96 | 79.99 | 99.95 | 17.75 | 79.98 | 97.73 | 2.214 |

| Margin: Expected Loss | 3.036 | 12.17 | 15.21 | 1.483 | 6.68 | 8.17 | 7.04 |

| Margin: Dist Ccoc | 20.55 | -5.35 | 15.21 | 13.94 | -5.77 | 8.17 | 7.04 |

| Margin: Dist PH | 12.94 | 2.269 | 15.21 | 6.32 | 3.506 | 9.82 | 5.38 |

| Margin: Dist Wang | 11.31 | 3.898 | 15.21 | 6.15 | 4.91 | 11.06 | 4.147 |

| Margin: Dist Dual | 9.72 | 5.49 | 15.21 | 6.47 | 5.94 | 12.4 | 2.803 |

| Margin: Dist Tvar | 8.74 | 6.47 | 15.21 | 6.65 | 6.5 | 13.15 | 2.053 |

| Margin: Dist Blend | 12.78 | 2.258 | 15.04 | 6.24 | 3.482 | 9.73 | 5.32 |

| Premium: Expected Loss | 22.99 | 92.16 | 115.15 | 19.23 | 86.67 | 105.9 | 9.25 |

| Premium: Dist Ccoc | 40.51 | 74.64 | 115.15 | 31.68 | 74.21 | 105.9 | 9.25 |

| Premium: Dist PH | 32.89 | 82.26 | 115.15 | 24.06 | 83.49 | 107.55 | 7.6 |

| Premium: Dist Wang | 31.26 | 83.89 | 115.15 | 23.89 | 84.9 | 108.79 | 6.36 |

| Premium: Dist Dual | 29.68 | 85.48 | 115.15 | 24.21 | 85.92 | 110.13 | 5.02 |

| Premium: Dist Tvar | 28.69 | 86.46 | 115.15 | 24.39 | 86.49 | 110.88 | 4.267 |

| Premium: Dist Blend | 32.74 | 82.25 | 114.99 | 23.99 | 83.47 | 107.46 | 7.53 |

| Loss Ratio: Expected Loss | 0.868 | 0.868 | 0.868 | 0.923 | 0.923 | 0.923 | 0.239 |

| Loss Ratio: Dist Ccoc | 0.493 | 1.072 | 0.868 | 0.56 | 1.078 | 0.923 | 0.239 |

| Loss Ratio: Dist PH | 0.607 | 0.972 | 0.868 | 0.738 | 0.958 | 0.909 | 0.291 |

| Loss Ratio: Dist Wang | 0.638 | 0.954 | 0.868 | 0.743 | 0.942 | 0.898 | 0.348 |

| Loss Ratio: Dist Dual | 0.673 | 0.936 | 0.868 | 0.733 | 0.931 | 0.887 | 0.441 |

| Loss Ratio: Dist Tvar | 0.696 | 0.925 | 0.868 | 0.728 | 0.925 | 0.881 | 0.519 |

| Loss Ratio: Dist Blend | 0.61 | 0.973 | 0.869 | 0.74 | 0.958 | 0.909 | 0.294 |

| Capital: Expected Loss | 30.36 | 121.69 | 152.05 | 14.83 | 66.85 | 81.68 | 70.37 |

| Capital: Dist Ccoc | 193.41 | -41.35 | 152.05 | 127.25 | -45.57 | 81.68 | 70.37 |

| Capital: Dist PH | 103.52 | 48.54 | 152.05 | 43.14 | 36.88 | 80.03 | 72.03 |

| Capital: Dist Wang | 92.18 | 59.87 | 152.05 | 35.78 | 43.01 | 78.79 | 73.26 |

| Capital: Dist Dual | 89.01 | 63.04 | 152.05 | 33.53 | 43.92 | 77.44 | 74.61 |

| Capital: Dist Tvar | 88.87 | 63.19 | 152.05 | 33.27 | 43.43 | 76.69 | 75.36 |

| Capital: Dist Blend | 103.52 | 48.7 | 152.21 | 43.12 | 37 | 80.12 | 72.09 |

| Rate of Return: Expected Loss | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

| Rate of Return: Dist Ccoc | 0.106 | 0.129 | 0.1 | 0.11 | 0.127 | 0.1 | 0.1 |

| Rate of Return: Dist PH | 0.125 | 0.047 | 0.1 | 0.146 | 0.095 | 0.123 | 0.075 |

| Rate of Return: Dist Wang | 0.123 | 0.065 | 0.1 | 0.172 | 0.114 | 0.14 | 0.057 |

| Rate of Return: Dist Dual | 0.109 | 0.087 | 0.1 | 0.193 | 0.135 | 0.16 | 0.038 |

| Rate of Return: Dist Tvar | 0.098 | 0.102 | 0.1 | 0.2 | 0.15 | 0.171 | 0.027 |

| Rate of Return: Dist Blend | 0.123 | 0.046 | 0.099 | 0.145 | 0.094 | 0.121 | 0.074 |

| Leverage: Expected Loss | 0.757 | 0.757 | 0.757 | 1.297 | 1.297 | 1.297 | 0.131 |

| Leverage: Dist Ccoc | 0.209 | -1.805 | 0.757 | 0.249 | -1.628 | 1.297 | 0.131 |

| Leverage: Dist PH | 0.318 | 1.695 | 0.757 | 0.558 | 2.264 | 1.344 | 0.105 |

| Leverage: Dist Wang | 0.339 | 1.401 | 0.757 | 0.668 | 1.974 | 1.381 | 0.087 |

| Leverage: Dist Dual | 0.333 | 1.356 | 0.757 | 0.722 | 1.956 | 1.422 | 0.067 |

| Leverage: Dist Tvar | 0.323 | 1.368 | 0.757 | 0.733 | 1.991 | 1.446 | 0.057 |

| Leverage: Dist Blend | 0.316 | 1.689 | 0.755 | 0.556 | 2.256 | 1.341 | 0.104 |

| Assets: Expected Loss | 53.36 | 213.85 | 267.2 | 34.06 | 153.52 | 187.58 | 79.62 |

| Assets: Dist Ccoc | 233.92 | 33.29 | 267.2 | 158.94 | 28.64 | 187.58 | 79.62 |

| Assets: Dist PH | 136.41 | 130.79 | 267.2 | 67.2 | 120.37 | 187.58 | 79.62 |

| Assets: Dist Wang | 123.44 | 143.76 | 267.2 | 59.67 | 127.91 | 187.58 | 79.62 |

| Assets: Dist Dual | 118.69 | 148.52 | 267.2 | 57.74 | 129.84 | 187.58 | 79.62 |

| Assets: Dist Tvar | 117.57 | 149.64 | 267.2 | 57.66 | 129.92 | 187.58 | 79.62 |

| Assets: Dist Blend | 136.26 | 130.95 | 267.2 | 67.11 | 120.47 | 187.58 | 79.62 |

Figure W

PIR Chapter 15, Figure 15.11, Loss and loss spectrums.

Figure X

PIR Chapter 15, Figures 15.12, 15.13, 15.14, Percentile layer of capital allocations by asset level.

Table Y

PIR Chapter 15, Tables 15.38, 15.39, 15.40, Percentile layer of capital allocations compared to distortion allocations.

| Method | Gross: Cat | Gross: NonCat | Gross: Total | Net: Cat | Net: NonCat | Net: Total | Ceded: Diff |

|---|---|---|---|---|---|---|---|

| Expected Loss | 53.36 | 213.8 | 267.2 | 34.06 | 153.5 | 187.6 | 79.62 |

| Dist Ccoc | 233.9 | 33.29 | 267.2 | 158.9 | 28.64 | 187.6 | 79.62 |

| Dist PH | 136.4 | 130.8 | 267.2 | 67.2 | 120.4 | 187.6 | 79.62 |

| Dist Wang | 123.4 | 143.8 | 267.2 | 59.67 | 127.9 | 187.6 | 79.62 |

| Dist Dual | 118.7 | 148.5 | 267.2 | 57.74 | 129.8 | 187.6 | 79.62 |

| Dist Tvar | 117.6 | 149.6 | 267.2 | 57.66 | 129.9 | 187.6 | 79.62 |

| Dist Blend | 136.3 | 130.9 | 267.2 | 67.11 | 120.5 | 187.6 | 79.62 |

| PLC | 113.2 | 154 | 267.2 | 54 | 133.6 | 187.6 | 79.62 |

Cat/Non-Cat Case Description

Cat/Non-Cat in the new syntax.

Distributions

# Line A (usually thinner tailed)

agg NonCat 1 claim sev gamma 80 cv 0.15 fixed

# Line B Gross (usually thicker tailed)

agg Cat 1 claim sev lognorm 20 cv 1.00 fixed

# Line B Net

agg Cat 1 claim sev lognorm 20 cv 1.00 fixed aggregate net of 79.640625 xs 41.109375Other Parameters

reg_p = 0.999roe = 0.1d2tc = 0.3s_values = [0.005, 0.01, 0.03]gs_values = [0.029126, 0.047619, 0.074074]f_discrete = Falselog2 = 16bs = 0.015625padding = 1

Description of Tables and Figures

| Ref. | Kind | Chapter | Number(s) | Description |

|---|---|---|---|---|

| A | Table | 2 | 2.3, 2.5, 2.6, 2.7 | Estimated mean, CV, skewness and kurtosis by line and in total, gross and net. |

| B | Figure | 2 | 2.2, 2.4, 2.6 | Gross and net densities on a linear and log scale. |

| C | Figure | 2 | 2.3, 2.5, 2.7 | Bivariate densities: gross and net with gross sample. |

| D | Figure | 4 | 4.9, 4.10, 4.11, 4.12 | TVaR, and VaR for unlimited and limited variables, gross and net. |

| E | Table | 4 | 4.6, 4.7, 4.8 | Estimated VaR, TVaR, and EPD by line and in total, gross, and net. |

| F | Table | 7 | 7.2 | Pricing summary. |

| G | Table | 7 | 7.3 | Details of reinsurance. |

| H | Table | 9 | 9.2, 9.5, 9.8 | Classical pricing by method. |

| I | Table | 9 | 9.3, 9.6, 9.9 | Sum of parts (SoP) stand-alone vs. diversified classical pricing by method. |

| J | Table | 9 | 9.4, 9.7, 9.10 | Implied loss ratios from classical pricing by method. |

| K | Table | 9 | 9.11 | Comparison of stand-alone and sum of parts premium. |

| L | Table | 9 | 9.12, 9.13, 9.14 | Constant CoC pricing by unit for Case Study. |

| M | Figure | 11 | 11.2, 11.3, 11.4,11.5 | Distortion envelope for Case Study, gross. |

| N | Table | 11 | 11.5 | Parameters for the six SRMs and associated distortions. |

| O | Figure | 11 | 11.6, 11.7, 11.8 | Variation in insurance statistics for six distortions as \(s\) varies. |

| P | Figure | 11 | 11.9, 11.10, 11.11 | Variation in insurance statistics as the asset limit is varied. |

| Q | Table | 11 | 11.7, 11.8, 11.9 | Pricing by unit and distortion for Case Study. |

| R | Table | 13 | 13.1 missing | Comparison of gross expected losses by Case, catastrophe-prone lines. |

| S | Table | 13 | 13.2, 13.3, 13.4 | Constant 0.10 ROE pricing for Case Study, classical PCP methods. |

| T | Figure | 15 | 15.2 - 15.7 (G/N) | Twelve plot. |

| U | Figure | 15 | 15.8, 15.9, 15.10 | Capital density by layer. |

| V | Table | 15 | 15.35, 15.36, 15.37 | Constant 0.10 ROE pricing for Cat/Non-Cat Case Study, distortion, SRM methods. |

| W | Figure | 15 | 15.11 | Loss and loss spectrums. |

| X | Figure | 15 | 15.12, 15.13, 15.14 | Percentile layer of capital allocations by asset level. |

| Y | Table | 15 | 15.38, 15.39, 15.40 | Percentile layer of capital allocations compared to distortion allocations. |