Conditional Expectations Given The Sum of Independent Random Variables with Regularly Varying Densities

notes

Summary of results and examples from a recent paper of Denuit et al.

Author

Stephen J. Mildenhall

Published

2024-04-04

This post summarizes results from the recent paper [1].

Assumptions

\(X\) and \(Y\) are independent random variables with regularly varying densities, \(f(x)=x^{-\alpha}L(x)\) for slowly varying \(L\). The tail indices are \(\alpha_X\) and \(\alpha_Y\). Assume \(\min(\alpha_X, \alpha_Y) >2\) so that \(X\) and \(Y\) have finite expectations.

\(S=X+Y\), \(m_X(s)=\mathsf E[X\mid S=s]\), and \(m_Y(s)=\mathsf E[Y\mid S=s]\).

In all these examples \(\alpha_Y \le \alpha_X\), meaning that \(Y\) is thicker tailed than \(X\).

Findings

Proposition 2.3.

If \(f_Y\) is ultimately decreasing and \(f_X\) is ultimately small compared to \(f_{X+Y}\) then \(\lim_s\inf m_X(s)\ge \mathsf E[X]\)

Property 3.1.

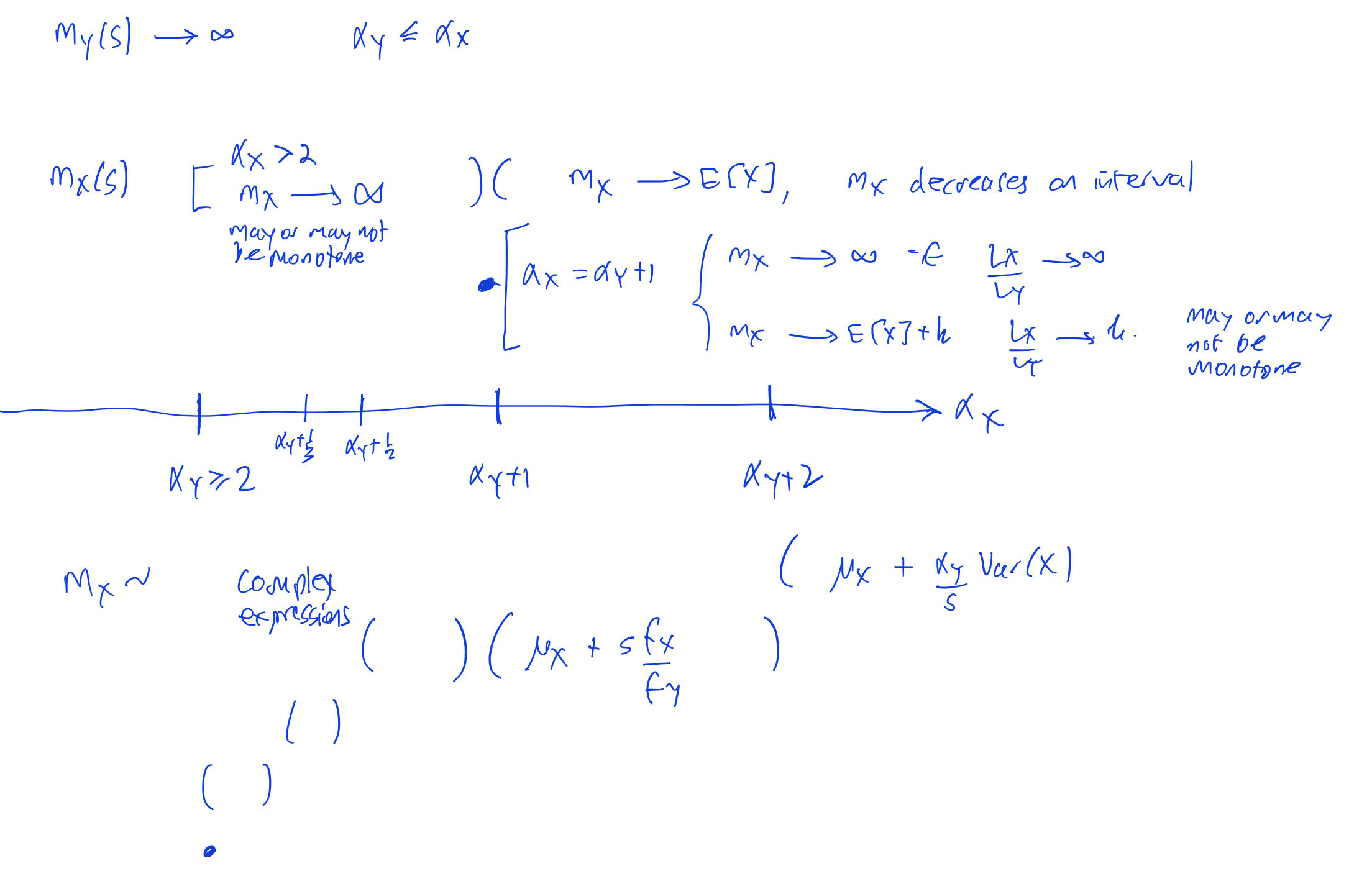

If \(\alpha_Y \le \alpha_X\) then \(m_Y(s)\to\infty\) as \(s\to\infty\), meaning the thicker tailed projection always tends to infinity.

Property 3.2.

If \(\alpha_X > \alpha_Y + 1\) then \(m_X(s) \to \mathsf E[X]\) as \(s\to\infty\).

Property 3.3.

In the case 3.2, there is a non-empty interval in \((0, \infty)\) where \(m_X\) is decreasing.

Property 3.5.

If second moments exist then \(\mathsf{cov}(m_X(S), m_Y(S))\ge 0\).

Property 3.5 means that “if there are values for which the monotonicity of \(m_X(·)\) and \(m_Y(·)\) differ, those must be values with small probability of occurrence or with slight differences in the increasing/decreasing rate, as in overall terms the dependence remains positive.”

Property 3.6.

If \(\alpha_X > 2\) and \(\alpha_Y \le \alpha_X < \alpha_Y + 1\) then \(m_X(s) \to \infty\) as \(s\to\infty\).

Property 3.9.

If \(\alpha_X = \alpha_Y + 1\) then

If \(L_X(s)/L_Y(s)\to\infty\) as \(s\to\infty\) then \(m_X(s)\to\infty\) as \(s\to\infty\).

If \(L_X(s)/L_Y(s) = k\) as \(s\to\infty\) then \(m_X(s)\to\mathsf E[X] + k\) as \(s\to\infty\).

In the case 3.9, \(m_X\) can be increasing.

Asymptotic Expansions

Section 4 gives asymptotic expansions for \(m_X\) in the corresponding cases.

Property 4.3.

If \(\alpha_X > \alpha_Y + 2\) then \[m_x(s) \sim \mu_X+\frac{\alpha_Y}{s}\mathsf{Var}(X).\]

Property 4.5.

If \(\alpha_Y + 2 > \alpha_X > \alpha_Y+1\) then \[m_x(s) \sim \mu_X+s \frac{f_X(s)}{f_X(s)}.\]

Property 4.7.

If _Y + 1 > _X > _Y$ then

If \(\alpha_X\in(\alpha_Y+1/2, \alpha_Y+1)\) then \[m_x(s) \sim s \frac{f_X}{f_X}\left( 1 + \mu_X\frac{f_Y}{sf_X} - \frac{f_X}{f_Y} \right).\]

If \(\alpha_X\in(\alpha_Y+1/3, \alpha_Y+1/2)\) then \[m_x(s) \sim s \frac{f_X}{f_X}\left( 1 - \frac{f_X}{f_Y} +\mu_X\frac{f_Y}{sf_X} \right).\]

If \(\alpha_X\in(\alpha_Y, \alpha_Y+1/3)\) then \[m_x(s) \sim s \frac{f_X}{f_X}\left( 1 - \frac{f_X}{f_Y}\left(1 - \frac{f_X}{f_Y}\right) \right).\]

Property 4.9.

If \(\alpha_Y = \alpha_X=\alpha\) and \(f_X\sim cf_Y\), then \[m_X(s)\sim \frac{c}{1+c}s\left(1+ \frac{1}{s}\left(\frac{\alpha}{1+c}(\mu_Y-\mu_X) + \frac{\mu_X}{c} - \mu_Y \right)\right).\]

The next figure lays out the various possible options.

Schematic of the different possible behaviors of \(m_X(s)\).

Examples

The paper provides examples for all the behaviors described by the different properties. It uses a parameterizations in terms of \(\alpha\) for clarity.

The examples below use aggregate with scipy.stats parameterization to illustrate the same behaviors.

Code to setup .

Code

import numpy as npfrom aggregate import build, knobble_fontsknobble_fonts(True)def example(aX, aY, lam, scale, mm, verbose): k = lam ** (aX - aY) * aX / aY port = build('port P 'f'agg X 1 claim sev {lam} * pareto {aX} - {lam} fixed 'f'agg Y 1 claim sev {lam} * pareto {aY} - {lam} fixed ' , normalize=False, log2=20, recommend_p=1-1e-13)if verbose: qd(port)# port.plot() l = port.q(0.999) * scale ax = port.density_df.loc[:l].filter(regex='exeqa_[XYt]').plot(figsize=(3,3)) ax.axhline(port.X.est_m, c='k', lw=.5, label=f'Mean X {port.X.est_m:.2f}')if aY +1== aX: ax.axhline(port.X.est_m + k, c='r', lw=.5, label=f'Mean X + k {k + port.X.est_m:.2f}') ax.set(ylim=[0, l], xlim=[0,l])# add asymptotic estimates s = np.array(port.density_df.loc[:l].index) fx = port.X.density_df.loc[:l].p_total fy = port.Y.density_df.loc[:l].p_total mx = port.X.agg_m sx = port.X.agg_var appx =None fxy = fx / fyif aX > aY +2:if verbose: print('more than 2') appx = mx + aY * sx / selif aY +2> aX > aY +1:if verbose: print('more than 1') appx = mx + s * fxyelif aY +1> aX > aY +0.5:if verbose: print('more than 0.5') appx = s * fxy * (1+ mx * fy / fx / s - fxy)elif aY +0.5> aX > aY +1/3:if verbose: print('more than 1/3') appx = s * fxy * (1- fxy + mx * fy / fx / s)elif aX < aY +1/3:if verbose: print('less than 1/3') appx = s * fxy * (1- fxy + fxy**2)if appx isnotNone: ax.plot(s, appx, ls='--', lw=1, label='Asymptotic expansion') ax.legend() ax.set(title=f'αX={aX}, αY={aY}, λ={lam}')if aX > aY +1: ax.set(ylim=[0, mm * port.X.est_m])else: ax.set(aspect='equal')

Figure 2: Same tail thickness, illustrating humped behavior, \(m_X\) diverges, parameters from paper Example 4.10.

Extensions

Section 5 extends sections 3 and 4 to the case of zero-augmented variables.

Section 6 considers sums of more than two variables. If the gap between the smallest smallest \(\alpha\) and the rest is more than 1 then \(m_i(s)\to\mathsf E[X_i]\) for all but the thickest tailed distribution (Proposition 6.2).

Schematic of the different possible behaviors of \(m_X(s)\).Figure 1 (a): Tails differ by 2.5, humped behavior tending to mean of \(X\).Figure 1 (b): Tails differ by 1.5, same behavior but different asymptotic expansion.Figure 1 (c): Tails differ by 1, \(k=1.333\) increasing to greater than mean.Figure 1 (d): Tails differ by 3/4, varying asymptotic expansion.Figure 1 (e): Tails differ by 2/5, varying asymptotic expansionFigure 1 (f): Tails differ by 1/4, varying asymptotic expansionFigure 2 (a): Equal scales.Figure 2 (b): Zoomed y scale.